In immediately’s article, we’ll be exploring double construction choice setups.

We’ll start with probably the most acquainted instance, the double calendar, then transfer on to the double butterfly, and eventually talk about a hybrid double configuration that mixes one butterfly with one calendar.

By the top of this text, you’ll perceive the variations amongst these three setups and when every is finest used.

All of them are non-directional trades, which implies we ideally need the underlying value to remain close to its present degree somewhat than transfer sharply in both path.

The good thing about the double construction is that it gives a large zone inside which the worth can transfer whereas nonetheless maintaining the place worthwhile.

Let’s check out the three key choice Greeks: theta, delta, and vega.

We all know that in all of those setups, theta is optimistic, that means the commerce earns revenue over time because the choices we promote decay quicker than those we purchase.

Since these methods are comparatively delta-neutral, the primary distinction between these constructions then turns into vega.

Contents

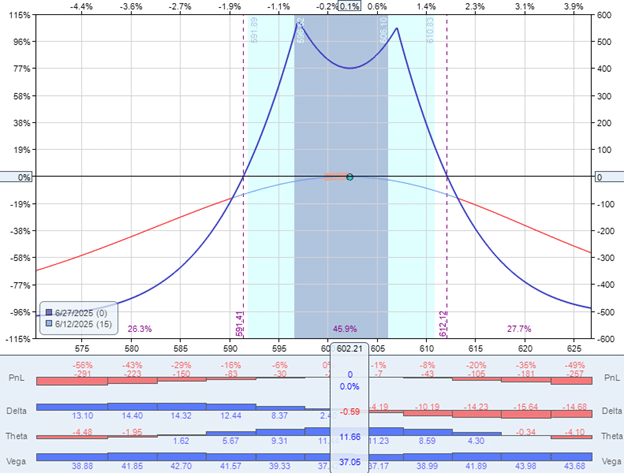

Right here is an instance of a double calendar on the S&P 500 ETF utilizing two contracts with about $500 of complete threat:

Date: June 12, 2025

Value: SPY @ $602.21

Promote two contracts June 27, SPY $607 callBuy two contracts July third, SPY $607 callSell two contracts June 27, SPY $597 putBuy two contracts July third, SPY $597 put

Internet debit: -$520

For this double calendar, the vega Greek is optimistic 37, as proven within the histogram above.

Which means that the place advantages when the implied volatility of the underlying will increase.

Due to this fact, this construction is nice when implied volatility is comparatively low.

Which means that when volatility is already close to the underside, a double calendar commerce is much less prone to lose worth from any additional decline in volatility.

VIX is a measure of the S&P 500 volatility.

On the time of this commerce, it’s at 17.6, a average degree.

A VIX between 12 and 15 could be thought of low.

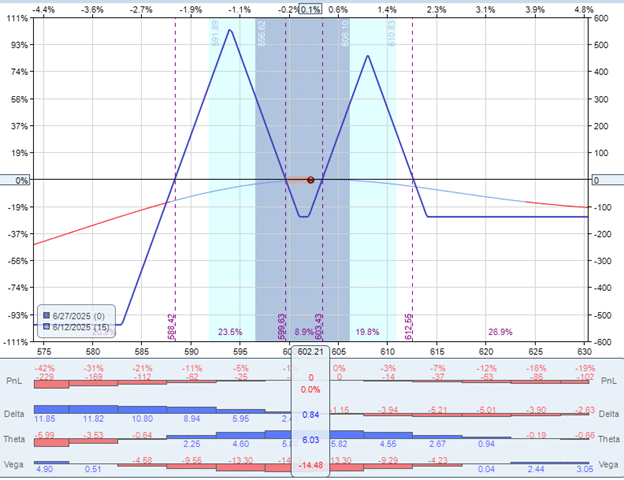

The double butterfly, then again, has damaging vega, that means it loses worth as volatility rises.

Date: June 12, 2025

Value: SPY @ $602.21

Name Butterfly:

Purchase one contract June 27, SPY $614 callSell two contracts June 27, SPY $608 callBuy one contract June 27, SPY $601 name

Debit: -$165

Put Butterfly

Purchase one contract June 27, SPY $602 putSell two contracts June 27 SPY $594 putBuy one contract June 27, SPY $583 put

Debit: -$75

As a result of there are six choice strikes (or six legs) on this commerce, we have to place this as two separate orders.

The general threat within the commerce is $539, or about $500, to make it akin to the calendar instance.

On this construction, vega is -14.

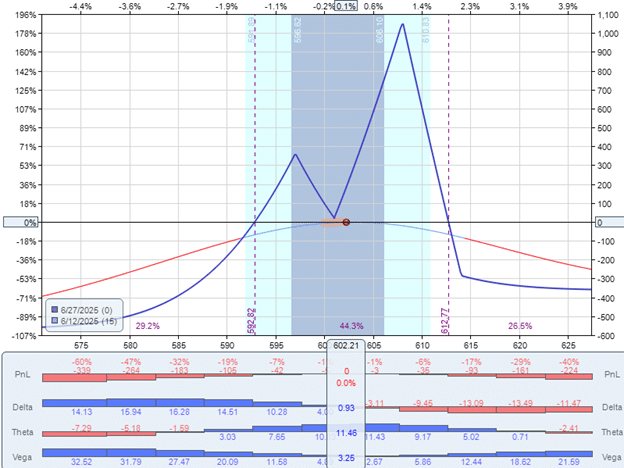

Now, for those who’re unsure in regards to the path of volatility, a hybrid mixture construction consisting of a calendar and a butterfly could also be extra acceptable.

Date: June 12, 2025

Value: SPY @ $602.21

Name Butterfly:

Purchase two contracts June 27, SPY $614 callSell 4 contracts June 27, SPY $608 callBuy two contracts June 27, SPY $601 name

Debit: -$330

Put Calendar:

Promote two contracts June 27 SPY $597 putBuy two contracts July third, SPY $597 put

Debit: -$233

On this setup, the butterfly carries damaging vega whereas the calendar has optimistic vega, serving to offset one another and lowering the construction’s total sensitivity to volatility modifications.

Its total vega is comparatively impartial at 3.

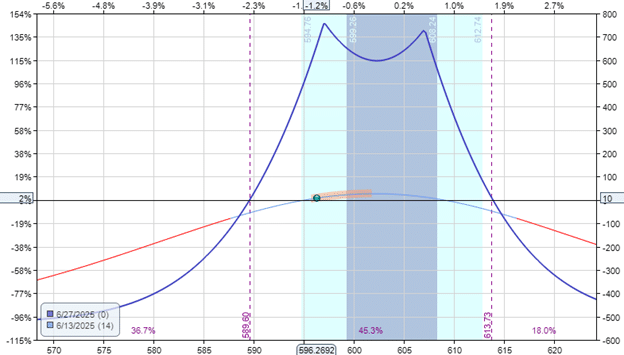

If you happen to take a look at the Greeks histogram within the above three constructions, you see that they’re configured to be delta-neutral inside plus or minus one delta.

The breakeven factors of the expiration graph are additionally about the identical for all three constructions.

That is the place the expiration graph crosses the zero-profit horizontal.

In our instances, the breakeven factors are $590 and $612.

If SPY falls in between these two costs at expiration, the commerce must be worthwhile.

The broader aside the breakeven factors, the upper the likelihood of success.

For constructions that comprise time spreads, resembling calendars, these breakeven factors can shift because the commerce progresses.

4 Ideas For Higher Iron Condors

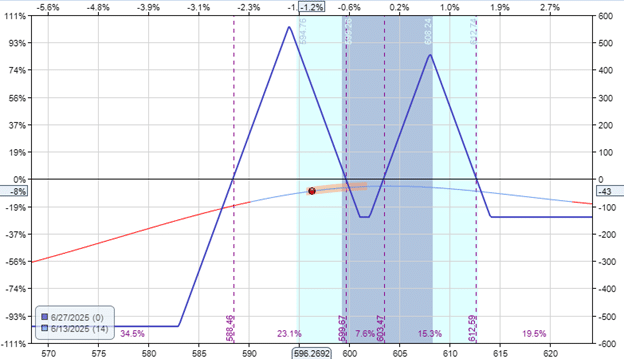

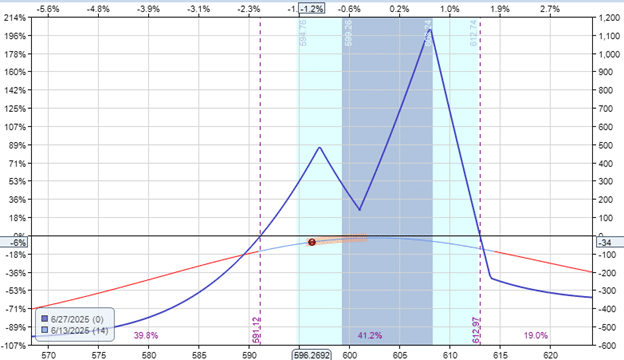

By the top of the next day, SPY dropped 6 factors to $596.27 – equal to a 60-point transfer within the SPX.

It’s not a extreme drop, however definitely noticeable.

Such strikes are sometimes accompanied by elevated volatility.

VIX went from 17.6 to 21.6.

The double calendar fared the perfect with a achieve of $10 as a result of it advantages partially from volatility will increase.

If you happen to examine the before-and-after snapshots of the mannequin, you see that the T+0 line rose.

And the expiration graph expanded, widening the breakeven factors barely.

The double-fly fared the worst, shedding -$43, as a result of it’s harm by rising volatility…

You see that its T+0 line had dropped beneath the zero-profit horizontal.

Its expiration graph and breakeven factors stay the identical, as they don’t change for constructions with all choices on the identical expiration date.

The hybrid construction’s result’s between the earlier two examples, with a loss -$34.

It had impartial vega and was not affected an excessive amount of by the change in volatility, as we are able to see that its T+0 line was precisely because it was earlier than.

Its loss is as a result of underlying’s value motion, as was the case with the opposite two constructions.

The double calendar’s volatility profit offset the loss from the worth transfer.

On the similar time, the elevated volatility exacerbated the loss on the double fly.

In abstract, understanding how vega behaves throughout completely different double constructions is essential for selecting the best technique in various volatility situations.

The double calendar thrives when volatility is low and anticipated to rise.

The double butterfly performs finest in environments with secure or declining volatility.

The hybrid construction presents a balanced strategy when volatility path is unsure.

It’s the construction that’s least delicate to volatility.

Merchants who need to hedge their directional and volatility threat whereas isolating their theta decay will need to think about the hybrid construction.

By aligning your commerce alternative with the market’s volatility outlook, you possibly can higher handle threat and enhance the consistency of your returns.

We hope you loved this text on evaluating double choices constructions.

If in case you have any questions, please ship an e-mail or depart a remark beneath.

Commerce protected!

Disclaimer: The knowledge above is for instructional functions solely and shouldn’t be handled as funding recommendation. The technique offered wouldn’t be appropriate for buyers who usually are not conversant in alternate traded choices. Any readers on this technique ought to do their very own analysis and search recommendation from a licensed monetary adviser.

")