By Aacashi Nawyndder and Vivek Krishnamoorthy

TL;DR

Bayesian statistics affords a versatile, adaptive framework for making buying and selling selections by updating beliefs with new market information. Not like conventional fashions, Bayesian strategies deal with parameters as chances, making them ideally suited for unsure, fast-changing monetary markets.

They’re utilized in danger administration, mannequin tuning, classification, and incorporating professional views or various information. Instruments like PyMC and Bayesian optimisation make it accessible for quants and merchants aiming to construct smarter, data-driven methods.

This weblog covers:

Need to ditch inflexible buying and selling fashions and really harness the facility of incoming market data? Think about a system that learns and adapts, similar to you do, however with the precision of arithmetic. Welcome to the world of Bayesian statistics, a game-changing framework for algorithmic merchants. It’s all about making knowledgeable selections by logically mixing what you already know with what the market is telling you proper now.

Let’s discover how this could sharpen your buying and selling edge!

This method contrasts with the standard, or “frequentist,” view of likelihood, which frequently sees chances as long-run frequencies of occasions and parameters as mounted, unknown constants (Neyman, 1937).

Bayesian statistics, however, treats parameters themselves as random variables about which we are able to have beliefs and replace them as extra information is available in (Gelman et al., 2013). Truthfully, this feels tailored for buying and selling, does not it? In any case, market circumstances and relationships are hardly set in stone. So, let’s bounce in and see how you need to use Bayesian stats to get a leg up within the fast-paced world of finance and algorithmic buying and selling.

Stipulations

To totally grasp the Bayesian strategies mentioned on this weblog, you will need to first set up a foundational understanding of likelihood, statistics, and algorithmic buying and selling.

For a conceptual introduction to Bayesian statistics, Bayesian Inference Strategies and Equation Defined with Examples affords an accessible rationalization of Bayes’ Theorem and the way it applies to uncertainty and decision-making, foundational to making use of Bayesian fashions in markets.

What You may Study:

The core concept behind Bayesian considering is updating beliefs with new proof.Understanding Bayes’ Theorem: your mathematical device for perception updating.Why Bayesian strategies are an important match for the uncertainties of monetary markets.Sensible examples of Bayesian statistics in algorithmic buying and selling:Estimating mannequin parameters that adapt to new information.Constructing easy predictive fashions (like Naive Bayes for market course).Incorporating professional views or various information into your fashions.The Execs, Cons, and Current Traits of Utilizing Bayesian Approaches in Quantitative Finance.

The Bayesian Fundamentals

Prior Beliefs, New Proof, Up to date Beliefs

Okay, let’s break down the elemental magic of Bayesian statistics. At its core, it is constructed on a splendidly easy but extremely highly effective concept: our understanding of the world is just not static; it evolves as we collect extra data.

Give it some thought like this: you’ve got acquired a brand new buying and selling technique you are mulling over.

Prior Perception (Prior Likelihood): Based mostly in your preliminary analysis, backtesting on historic information, or perhaps a hunch, you’ve some preliminary perception about how worthwhile this technique could be. To illustrate you assume there is a 60% likelihood will probably be worthwhile. That is your prior.New Proof (Chance): You then deploy the technique on a small scale or observe its hypothetical efficiency over a number of weeks of dwell market information. This new information is your proof. The probability perform tells you the way possible this new proof is, given completely different underlying states of the technique’s true profitability.Up to date Perception (Posterior Likelihood): After observing the brand new proof, you replace your preliminary perception. If the technique carried out properly, your confidence in its profitability would possibly enhance from 60% to, say, 75%. If it carried out poorly, it would drop to 40%. This up to date perception is your posterior.

This entire strategy of tweaking your beliefs based mostly on new information is neatly wrapped up and formalised by what known as the Bayes’ Theorem.

Bayes’ Theorem: The Engine of Bayesian Studying

So, Bayes’ Theorem is the precise formulation that ties all these items collectively. When you’ve got a speculation (let’s name it H) and a few proof (E), the concept appears like this:

Bayes’ Theorem:

( P(H mid E) = frac{P(E mid H) cdot P(H)}{P(E)} )

The place:

P(H|E) is the Posterior Likelihood: The likelihood of your speculation (H) being true after observing the proof (E). That is what you need to calculate; your up to date perception.

P(E|H) is the Chance: The likelihood of observing the proof (E) in case your speculation (H) have been true. For instance, in case your speculation is “this inventory is bullish,” how seemingly is it to see a 2% value enhance right now?

P(H) is the Prior Likelihood: The likelihood of your speculation (H) being true earlier than observing the brand new proof (E). That is your preliminary perception.

P(E) is the Likelihood of the Proof (additionally known as Marginal Chance or Normalising Fixed): The general likelihood of observing the proof (E) underneath all potential hypotheses. It is calculated by summing (or integrating) P(E|H) × P(H) over each potential H. This ensures the posterior chances sum as much as 1.

Let’s attempt to make this much less summary with a fast buying and selling state of affairs.

Instance: Is a Information Occasion Bullish for a Inventory?

Suppose an organization is about to launch an earnings report.

Speculation (H): The earnings report shall be considerably higher than anticipated (a “optimistic shock”).

Prior P(H): Based mostly on analyst chatter and up to date sector efficiency, you consider there is a 30% likelihood of a optimistic shock. So, P(H) = 0.30.

Proof (E): Within the hour earlier than the official announcement, the inventory value jumps 1%.

Chance P(E|H): from previous expertise that if there is a genuinely optimistic shock brewing, there is a 70% likelihood of seeing such a pre-announcement value bounce on account of insider data or some sharp merchants catching on early. So, P(E|H) = 0.70.

Likelihood of Proof P(E): This one’s a little bit extra concerned as a result of the value might bounce for different causes, too, proper? Perhaps the entire market is rallying, or it is only a false hearsay. To illustrate:

The likelihood of the value bounce if it is a optimistic shock (P(E|H)) is 0.70 (as above).

The likelihood of the value bounce if it is not a optimistic shock (P(E|not H)) is, say, 0.20 (it is much less seemingly, however potential).

Since P(H) = 0.30, then P(not H) = 1 – 0.30 = 0.70.

So, P(E) = P(E|H)P(H) + P(E|not H)P(not H) = (0.70 * 0.30) + (0.20 * 0.70) = 0.21 + 0.14 = 0.35.

Now we are able to calculate the Posterior ( P(H mid E) ):

( P(H mid E) = frac{0.70 instances 0.30}{0.35} = frac{0.21}{0.35} = 0.60 )

Growth! After seeing that 1% value bounce, your perception that the earnings report shall be a optimistic shock has shot up from 30% to 60%! This up to date likelihood can then inform your buying and selling choice, maybe you are now extra inclined to purchase the inventory or regulate an present place.

After all, this can be a super-simplified illustration. Actual monetary fashions are juggling a considerably larger variety of variables and way more advanced likelihood distributions. However the stunning factor is, that core logic of updating your beliefs as new information is available in? That stays precisely the identical.

Supply

Why Bayesian Statistics Shines in Algorithmic Buying and selling

Monetary markets are a wild journey, filled with uncertainty, consistently altering relationships (non-stationarity, if you wish to get technical), and infrequently, not a variety of information for these actually uncommon, out-of-the-blue occasions. Bayesian strategies supply a number of benefits on this atmosphere:

Handles Uncertainty Like a Professional: Bayesian statistics does not simply offer you a single quantity; it naturally offers with uncertainty through the use of likelihood distributions for parameters, as a substitute of pretending they’re mounted, recognized values (Bernardo & Smith, 2000). This offers you a way more real looking image of what would possibly occur.Updating Beliefs with New Knowledge: Algorithmic buying and selling programs consistently course of new market information. Bayesian updating permits fashions to adapt dynamically. As an example, the volatility of an asset is not fixed; a Bayesian mannequin can replace its volatility estimate as new value ticks arrive.Working with Small Knowledge Units: Conventional frequentist strategies typically require massive pattern sizes for dependable estimates. Bayesian strategies, nevertheless, can provide you fairly wise insights even with restricted information, as a result of they allow you to usher in “informative priors” – principally, your present information from consultants, related markets, or monetary theories (Ghosh et al., 2006). It is a lifesaver whenever you’re making an attempt to mannequin uncommon occasions or new property that do not have an extended historical past.Mannequin Comparability and Averaging: Bayesian strategies present a extremely stable means (e.g., utilizing Bayes components or posterior predictive checks) to check completely different fashions and even common out their predictions. This typically results in extra strong and dependable outcomes (Hoeting et al., 1999).Lets You Weave in Qualitative Insights: Acquired a robust financial motive why a sure parameter ought to in all probability fall inside a selected vary? Priors offer you a proper option to combine that sort of qualitative hunch or professional opinion along with your arduous quantitative information.Clearer Interpretation of Chances: When a Bayesian mannequin tells you “there is a 70% likelihood this inventory will go up tomorrow,” it means precisely what it feels like: it’s your present diploma of perception. This could be a lot extra easy to behave on than making an attempt to interpret p-values or confidence intervals alone (Berger & Berry, 1988).

Sensible Bayesian Functions in Algorithmic Buying and selling

Alright, sufficient concept! Let’s get right down to brass tacks. How will you truly use Bayesian statistics in your buying and selling algorithms?

1. Adaptive Parameter Estimation: Holding Your Fashions Recent

So many buying and selling fashions lean closely on parameters – just like the lookback window in your shifting common, the velocity of imply reversion in a pairs buying and selling setup, or the volatility guess in an choices pricing mannequin. However right here’s the catch: market circumstances are at all times shifting, so parameters that have been golden yesterday could be suboptimal right now.

That is the place Bayesian strategies are tremendous useful. They allow you to deal with these parameters not as mounted numbers, however as distributions that get up to date as new information rolls in. Think about you are estimating the common every day return of a inventory.

Prior: You would possibly begin with a imprecise prior concept(e.g., a traditional distribution centred round 0 with a large unfold (customary deviation)) or a extra educated guess based mostly on how related shares within the sector have carried out traditionally.Chance: As every new buying and selling day supplies a return, you calculate the probability of observing that return given completely different potential values of the true common every day return.Posterior: Bayes’ theorem combines the prior and probability to provide you an up to date distribution for the common every day return. This posterior turns into the prior for the following day’s replace.It is a steady studying loop!

Sizzling Development Alert: Methods like Kalman Filters (that are inherently Bayesian) are extensively used for dynamically estimating unobserved variables, just like the “true” underlying value or volatility, in noisy market information (Welch & Bishop, 2006). One other space is Bayesian regression, the place the regression coefficients (e.g., the beta of a inventory) are usually not mounted factors however distributions that may evolve.For extra on regression in buying and selling, you would possibly need to take a look at how Regression is Utilized in Buying and selling.

Simplified Python Instance: Updating Your Perception a couple of Coin’s Equity (Assume Market Ups and Downs)

To illustrate we need to get a deal with on the likelihood of a inventory value going up (we’ll name it ‘Heads’) on any given day. It is a bit like making an attempt to determine if a coin is honest or biased.

Python Code:

Output:

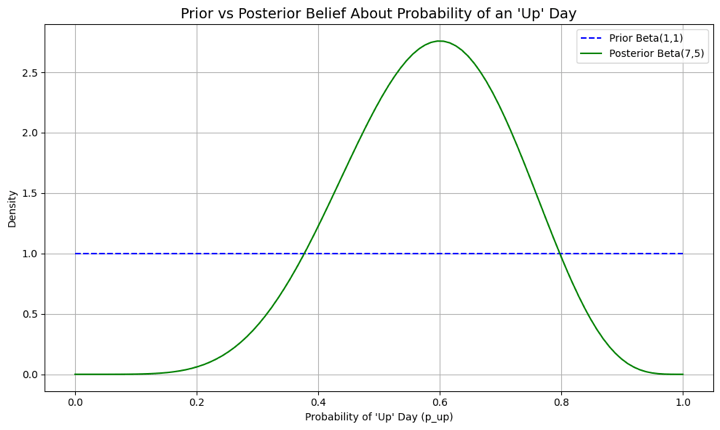

Preliminary Prior: Alpha=1, Beta=1

Noticed Knowledge: 6 ‘up’ days, 4 ‘down’ days

Posterior Perception: Alpha=7, Beta=5

Up to date Estimated Likelihood of an ‘Up’ Day: 0.58

95% Credible Interval for p_up: (0.31, 0.83)

On this code:

We begin off with a Beta(1,1) prior, which is uniform and suggests any likelihood of an ‘up’ day is equally seemingly.Then, we observe 10 days of market information with 6 ‘up’ days.The posterior distribution turns into Beta(1+6, 1+4) = Beta(7, 5).Our new level estimate for the likelihood of an ‘up’ day is 7 / (7+5) = 0.58, or 58%.The credible interval provides us a spread of believable values.

The graph supplies a transparent visible for this belief-updating course of. The flat blue line represents our preliminary, uninformative prior, the place any likelihood for an ‘up’ day was thought-about equally seemingly. In distinction, the orange curve is the posterior perception, which has been sharpened and knowledgeable by the noticed market information. The height of this new curve, centered round 0.58, represents our up to date, most possible estimate, whereas its extra concentrated form signifies our decreased uncertainty now that we now have proof to information us.

It is a toy instance, however it reveals the mechanics of how beliefs get up to date. In algorithmic buying and selling, this could possibly be utilized to the likelihood of a worthwhile commerce for a given sign or the likelihood of a market regime persisting.

2. Naive Bayes Classifiers for Market Prediction: Easy however Surprisingly Sensible!

Subsequent up, let’s speak about Naive Bayes. It is a easy probabilistic classifier that makes use of Bayes’ theorem, however with a “naive” (or for instance, optimistic) assumption that every one your enter options are unbiased of one another. Regardless of its simplicity, it may be surprisingly efficient for duties like classifying whether or not the following day’s market motion shall be ‘Up’, ‘Down’, or ‘Sideways’ based mostly on present indicators. (Rish, 2001)

Right here’s the way it works (conceptually):

Outline Options: These could possibly be technical indicators (e.g., RSI < 30, MACD crossover), value patterns (e.g., yesterday was an engulfing candle), and even sentiment scores from monetary information.

Gather Coaching Knowledge: Collect historic information the place you’ve these options and the precise consequence (Up/Down/Sideways).

Calculate Chances from Coaching Knowledge:

Prior Chances of Outcomes: P(Up), P(Down), P(Sideways) – merely the frequency of those outcomes in your coaching set.

Chance of Options given Outcomes: P(Feature_A | Up), P(Feature_B | Up), and so on. As an example, “What is the likelihood RSI < 30, given the market went Up the following day?”

Make a Prediction: For brand spanking new information (right now’s options):

Calculate the posterior likelihood for every consequence:

P(Up | Options) ∝ P(Up) * P(Feature_A | Up) * P(Feature_B | Up) * …

P(Down | Options) ∝ P(Down) * P(Feature_A | Down) * P(Feature_B | Down) * …

(And equally for Sideways)

The end result with the best posterior likelihood is your prediction.

Python Snippet Thought (Only a idea, you’d want sklearn for this):

Python Code:

Output:

Naive Bayes Classifier Accuracy (on dummy information): 0.43

This accuracy rating of 0.43 signifies the mannequin appropriately predicted the market’s course 43% of the time on the unseen take a look at information. Since this result’s beneath 50% (the equal of random likelihood), it means that, with the present dummy information and options, the mannequin doesn’t display predictive energy. In a real-world utility, such a rating would sign that the chosen options or the mannequin itself might not be appropriate, prompting a re-evaluation of the method or additional characteristic engineering.

This little snippet provides you the fundamental stream. Constructing an actual Naive Bayes classifier for buying and selling takes cautious thought of which options to make use of (that is “characteristic engineering”) and rigorous testing (validation). That “naive” assumption that every one options are unbiased won’t be completely true within the messy, interconnected world of markets, however it typically provides you a surprisingly good place to begin or baseline mannequin.Interested in the place to study all this? Don’t fear, pal, we’ve acquired you lined! Take a look at this course.

3. Bayesian Threat Administration (e.g., Worth at Threat – VaR)

You have in all probability heard of Worth at Threat (VaR), it is a widespread option to estimate potential losses. However conventional VaR calculations can typically be a bit static or depend on simplistic assumptions. Bayesian VaR permits for the incorporation of prior beliefs about market volatility and tail danger, and these beliefs might be up to date as new market shocks happen. This could result in danger estimates which can be extra responsive and strong, particularly when markets get uneven.

As an example, if a “black swan” occasion happens, a Bayesian VaR mannequin can adapt its parameters way more shortly to replicate this new, higher-risk actuality. A purely historic VaR, however, would possibly take rather a lot longer to catch up.

4. Bayesian Optimisation for Discovering Goldilocks Technique Parameters

Discovering these “excellent” parameters in your buying and selling technique (like the right entry/exit factors or the best lookback interval) can really feel like trying to find a needle in a haystack. Bayesian optimisation is a critically highly effective approach that may assist right here. It cleverly makes use of a probabilistic mannequin (typically a Gaussian Course of) to mannequin the target perform (like how worthwhile your technique is for various parameters) and selects new parameter units to check in a means that balances exploration (making an attempt new areas) and exploitation (refining recognized good areas) (Snoek et al., 2012). This may be way more environment friendly than simply making an attempt each mixture (grid search) or selecting parameters at random.

Sizzling Development Alert:Bayesian optimisation is a rising star within the broader machine studying world and is extremely well-suited for fine-tuning advanced algorithmic buying and selling methods, particularly when working every backtest takes a variety of computational horsepower.

5. Weaving in Different Knowledge and Professional Hunches (Opinions)

As of late, quants are more and more taking a look at “various information” sources, issues like satellite tv for pc photographs, the final temper on social media, or bank card transaction tendencies. Bayesian strategies offer you a extremely pure option to combine such various and infrequently unstructured information with conventional monetary information. You possibly can set your priors based mostly on how dependable or robust you assume the sign from an alternate information supply is.

And it is not nearly new information varieties. What if a seasoned portfolio supervisor has a robust conviction a couple of specific sector due to some geopolitical growth that is tough to quantify? That “professional opinion” can truly be formalised into a previous distribution, permitting it to affect the mannequin’s output proper alongside the purely data-driven alerts.

Current Business Buzz in Bayesian Algorithmic Buying and selling

Whereas Bayesian strategies have been round in finance for some time, a number of areas are actually heating up and getting a variety of consideration these days:

Bayesian Deep Studying (BDL): You understand how conventional deep studying fashions offer you a single prediction however do not actually inform you how “certain” they’re? BDL is right here to vary that! It combines the facility of deep neural networks with Bayesian ideas to provide predictions with related uncertainty estimates (Neal, 1995; Gal & Ghahramani, 2016). That is essential for monetary purposes the place figuring out the mannequin’s confidence is as necessary because the prediction itself. For instance, think about a BDL mannequin not simply predicting a inventory value, but in addition saying it is “80% assured the value will land between X and Y”.Probabilistic Programming Languages (PPLs): Languages like Stan, PyMC3 (Salvatier et al., 2016), and TensorFlow Likelihood are making it simpler for quants to construct and estimate advanced Bayesian fashions with out getting slowed down within the low-level mathematical particulars of inference algorithms like Markov Chain Monte Carlo (MCMC). This simpler entry is de facto democratising the usage of subtle Bayesian strategies throughout the board (Carpenter et al., 2017).Subtle MCMC and Variational Inference: As our fashions get extra bold, the computational grunt work wanted to suit them additionally grows. Fortunately, researchers are consistently cooking up extra environment friendly MCMC algorithms (like Hamiltonian Monte Carlo) and speedier approximate strategies like Variational Inference (VI) (Blei et al., 2017), making bigger Bayesian fashions tractable for real-world buying and selling.If you wish to study extra about MCMC, QuantInsti has a wonderful weblog on Introduction to Monte Carlo Evaluation.Dynamic Bayesian Networks for Recognizing Market Regimes: Monetary markets typically appear to flip between completely different “moods” or “regimes”, assume high-volatility vs. low-volatility intervals, or bull vs. bear markets. Dynamic Bayesian Networks (DBNs) can mannequin these hidden market states and the chances of transitioning between them, permitting methods to adapt their conduct accordingly (Murphy, 2002).

The Upsides and Downsides: What to Preserve in Thoughts

Like every highly effective device, Bayesian strategies include their very own set of professionals and cons.

Benefits:

Intuitive framework for updating beliefs.Quantifies uncertainty straight.Works properly with restricted information through the use of priors.Permits incorporation of professional information.Supplies a coherent option to evaluate and mix fashions.

Limitations:

Alternative of Prior: The choice of a previous might be subjective and may considerably affect the posterior, particularly with small datasets. A poorly chosen prior can result in poor outcomes. Whereas strategies for “goal” or “uninformative” priors exist, their appropriateness is usually debated.Computational Price: For advanced fashions, estimating the posterior distribution (particularly utilizing MCMC strategies) might be computationally intensive and time-consuming, which could be a constraint for high-frequency buying and selling purposes.Mathematical Complexity: Whereas PPLs are useful, a stable understanding of likelihood concept and Bayesian ideas remains to be wanted to use these strategies appropriately and interpret outcomes.

Continuously Requested Questions

Q. What makes Bayesian statistics completely different from conventional (frequentist) strategies in buying and selling?Bayesian statistics treats mannequin parameters as random variables with a and permits beliefs to be up to date with new information. In distinction, frequentist strategies assume parameters are mounted and require massive information samples. Bayesian considering is extra dynamic and well-suited to the non-stationary, unsure nature of monetary markets.

Q. How does Bayes’ Theorem assist in buying and selling selections? Are you able to give an instance?Bayes’ Theorem is used to replace chances based mostly on new market data. For instance, if a inventory value jumps 1% earlier than earnings, and previous information suggests this typically precedes a optimistic shock, Bayes’ Theorem helps revise your confidence in that speculation, turning a 30% perception into 60%, which may straight affect your commerce.

Q. What are priors and posteriors in Bayesian fashions, and why do they matter in finance?A previous displays your preliminary perception (from previous information, concept, or professional views), whereas a posterior is the up to date perception after contemplating new proof. Priors assist enhance efficiency in low-data or high-uncertainty conditions and permit integration of different information or human instinct in monetary modelling.

Q. What forms of buying and selling issues are greatest suited to Bayesian strategies?Bayesian strategies are perfect for:

Parameter estimation that adapts (instance, volatility, beta, shifting common lengths)Market regime detection utilizing dynamic Bayesian networksRisk administration (instance, Bayesian VaR)Technique optimisation utilizing Bayesian OptimisationClassification duties with Naive Bayes modelsThese approaches assist construct extra responsive and strong methods.

Q. Can Bayesian strategies work with restricted or noisy market information?Sure! Bayesian strategies shine in low-data environments by incorporating informative priors. Additionally they deal with uncertainty naturally, representing beliefs as distributions fairly than mounted values, essential when modelling uncommon market occasions or new property.

Q. How is Bayesian optimisation utilized in buying and selling technique design?Bayesian optimisation is used to tune technique parameters (like entry/exit thresholds) effectively. As a substitute of brute-force grid search, it balances exploration and exploitation utilizing a probabilistic mannequin (instance, Gaussian Processes), making it good for expensive backtesting environments.

Q. Are easy fashions like Naive Bayes actually helpful in buying and selling?Sure, Naive Bayes classifiers can function light-weight baseline fashions to foretell market course utilizing indicators like RSI, MACD, or sentiment scores. Whereas the belief of unbiased options is simplistic, these fashions can supply quick and surprisingly stable predictions, particularly with well-engineered options.

Q. How does Bayesian considering improve danger administration?Bayesian fashions, like Bayesian VaR (a, replace danger estimates dynamically as new information (or shocks) arrive, not like static historic fashions. This makes them extra adaptive to unstable circumstances, particularly throughout uncommon or excessive occasions.

Q. What instruments or libraries are used to construct Bayesian buying and selling fashions?Well-liked instruments embody:

PyMC and PyMC3 (Python)Stan (through R or Python)TensorFlow ProbabilityThese assist strategies like MCMC and variational inference, enabling the event of the whole lot from easy Bayesian regressions to Bayesian deep studying fashions.

Q. How can I get began with Bayesian strategies in buying and selling?Begin with small tasks:

Check a Naive Bayes classifier on market course.Use Bayesian updating for a method’s win fee estimation.Strive parameter tuning with Bayesian optimisation.Then discover extra superior purposes and contemplate studying sources corresponding to Quantra’s programs on machine studying in buying and selling and EPAT for a complete algo buying and selling program with Bayesian strategies.

Conclusion: Embrace the Bayesian Mindset for Smarter Buying and selling!

So, there you’ve it! Bayesian statistics affords an extremely highly effective and versatile option to navigate the unavoidable uncertainties that include monetary markets. By supplying you with a proper option to mix your prior information with new proof because it streams in, it helps merchants and quants construct algorithmic methods which can be extra adaptive, strong, and insightful.

Whereas it is not a magic bullet, understanding and making use of Bayesian ideas may help you progress past inflexible assumptions and make extra nuanced, probability-weighted selections. Whether or not you are tweaking parameters, classifying market circumstances, keeping track of danger, or optimising your total technique, the Bayesian method encourages a mindset of steady studying, and that’s completely very important for long-term success within the consistently shifting panorama of algorithmic buying and selling.

Begin small, maybe by experimenting with how priors impression a easy estimation, or by making an attempt out a Naive Bayes classifier. As you develop extra comfy, the wealthy world of Bayesian modeling will open up new avenues for enhancing your buying and selling edge.

When you’re critical about taking your quantitative buying and selling abilities to the following stage, contemplate Quantra’s specialised programs like “Machine Studying & Deep Studying for Buying and selling” to reinforce Bayesian strategies, or EPAT for complete, industry-leading algorithmic buying and selling certification. These equip you to sort out advanced markets with a big edge.

Continue learning, hold experimenting!

Additional Studying

For a structured and utilized studying path with Quantra, begin with Python for Buying and selling: Primary, then transfer to Technical Indicators Methods in Python.

For machine studying, discover the Machine Studying & Deep Studying in Buying and selling: Inexperienced persons studying monitor, which supplies sensible hands-on insights into implementing fashions like Bayesian classifiers in monetary markets.

When you’re a critical learner, you’ll be able to take the Government Programme in Algorithmic Buying and selling (EPAT), which covers statistical modelling, machine studying, and superior buying and selling methods with Python.

References

Neyman, J. (1937). Define of a concept of statistical estimation based mostly on the classical concept of likelihood. Philosophical Transactions of the Royal Society of London. Collection A, Mathematical and Bodily Sciences, 236(767), 333-380.https://royalsocietypublishing.org/doi/10.1098/rsta.1937.0005Gelman, A., Carlin, J. B., Stern, H. S., Dunson, D. B., Vehtari, A., & Rubin, D. B. (2013). Bayesian Knowledge Evaluation (third ed.). CRC Press.https://www.routledge.com/Bayesian-Knowledge-Evaluation/Gelman-Carlin-Stern-Dunson-Vehtari-Rubin/p/e-book/9781439840955Bernardo, J. M., & Smith, A. F. M. (2000). Bayesian Principle. John Wiley & Sons.https://onlinelibrary.wiley.com/doi/e-book/10.1002/9780470316870Ghosh, J. Okay., Delampady, M., & Samanta, T. (2006). An Introduction to Bayesian Evaluation: Principle and Strategies. Springer.http://ndl.ethernet.edu.et/bitstream/123456789/58197/1/41percent20pdf.pdfHoeting, J. A., Madigan, D., Raftery, A. E., & Volinsky, C. T. (1999). Bayesian mannequin averaging: A tutorial. Statistical Science, 14(4), 382-417.https://www.stat.colostate.edu/~jah/papers/statsci.pdfBerger, J. O., & Berry, D. A. (1988). Statistical evaluation and the phantasm of objectivity. American Scientist, 76(2), 159-165.https://www.medication.mcgill.ca/epidemiology/Joseph/programs/widespread/Berger.Berry.pdfWelch, G., & Bishop, G. (2006). An introduction to the Kalman filter. TR 95-041, College of North Carolina at Chapel Hill, Division of Pc Science.https://www.cs.unc.edu/~welch/media/pdf/kalman_intro.pdfRish, I. (2001, August). An empirical examine of the naive Bayes classifier. In IJCAI 2001 workshop on empirical strategies in synthetic intelligence (Vol. 3, No. 22, pp. 41-46).https://www.researchgate.web/publication/228845263_An_Empirical_Study_of_the_Naive_Bayes_ClassifierSnoek, J., Larochelle, H., & Adams, R. P. (2012). Sensible Bayesian optimization of machine studying algorithms. Advances in neural data processing programs, 25.https://papers.nips.cc/paper_files/paper/2012/hash/05311655a15b75fab86956663e1819cd-Summary.htmlNeal, R. M. (1995). Bayesian studying for neural networks. (Doctoral dissertation, College of Toronto).https://glizen.com/radfordneal/ftp/thesis.pdfGal, Y., & Ghahramani, Z. (2016). Dropout as a Bayesian approximation: Representing mannequin uncertainty in deep studying. Within the Worldwide Convention on machine studying (pp. 1050-1059). PMLR.https://proceedings.mlr.press/v48/gal16.htmlSalvatier, J., Wiecki, T. V., & Fonnesbeck, C. (2016). Probabilistic programming in Python utilizing PyMC3. PeerJ Pc Science, 2, e55.https://peerj.com/articles/cs-55/Carpenter, B., Gelman, A., Hoffman, M. D., Lee, D., Goodrich, B., Betancourt, M., … & Riddell, A. (2017). Stan: A probabilistic programming language. Journal of Statistical Software program, 76(1), 1-32.https://www.jstatsoft.org/article/view/v076i01Blei, D. M., Kucukelbir, A., & McAuliffe, J. D. (2017). Variational inference: A assessment for statisticians. Journal of the American Statistical Affiliation, 112(518), 859-877. https://www.tandfonline.com/doi/full/10.1080/01621459.2017.1285773Murphy, Okay. P. (2002). Dynamic Bayesian Networks: Illustration, Inference and Studying. (Doctoral dissertation, College of California, Berkeley).https://www.cs.ubc.ca/~murphyk/Thesis/thesis.html

Disclaimer: This weblog put up is for informational and academic functions solely. It doesn’t represent monetary recommendation or a advice to commerce any particular property or make use of any particular technique. All buying and selling and funding actions contain important danger. All the time conduct your personal thorough analysis, consider your private danger tolerance, and contemplate looking for recommendation from a certified monetary skilled earlier than making any funding selections.

")