Brief-Time period Correlated Stress Reversal Buying and selling

Brief-term reversal methods in U.S. large-cap fairness indexes, such because the S&P 500, are well-documented and broadly adopted. These reversals typically happen in response to transient intervals of market stress, the place sharp declines are adopted by fast recoveries (as we now have skilled in the previous couple of weeks). Conventional approaches sometimes determine such stress intervals utilizing solely the worth motion of the fairness index itself. On this analysis, nonetheless, we discover a broader perspective—one which leverages the habits of different asset lessons, together with gold, oil, and intermediate-term U.S. Treasuries. We display that utilizing alerts from these correlated property to detect stress occasions can improve the timing and robustness of reversal trades in equities. Moreover, we present that combining alerts throughout a number of markets results in a simpler and diversified reversal technique.

This examine proposes a novel method to analyzing the habits of main asset lessons throughout correlated stress occasions, with implications for portfolio administration and danger mitigation methods. Our analysis focuses on stress occasions that concurrently influence a number of asset lessons, particularly cases the place equities and commodities expertise concurrent declines whereas fixed-income securities carry out nicely.

Market stress occasions are sometimes characterised by sharp, synchronized actions throughout a number of asset lessons. When equities, commodities (reminiscent of oil or gold), and different dangerous property decline in tandem, it may sign a broader flight to security, sometimes accompanied by a rally in safer property like U.S. Treasuries (e.g., IEF). These co-movements might point out a short lived liquidity shock or a surge in danger aversion fairly than a shift in elementary worth. By figuring out days when a number of dangerous property fall concurrently—or when a dangerous asset declines whereas Treasuries rally—the technique goals to seize these short-term dislocations. Such alerts are extra strong indicators of a market overreaction or panic promoting than a decline in equities alone.

The rationale is that remoted declines in SPY or different single property might consequence from asset-specific information or technical elements. Nevertheless, concurrent declines throughout asset lessons—particularly when paired with a rally in authorities bonds—counsel systemic stress or correlated de-risking throughout portfolios. Such a multi-asset affirmation will increase the chance that markets have overshot within the quick time period, making a extra favorable entry level for mean-reversion methods. In essence, this method makes use of cross-asset consensus to filter for higher-conviction alternatives to behave as a liquidity supplier throughout momentary dislocations.

Information

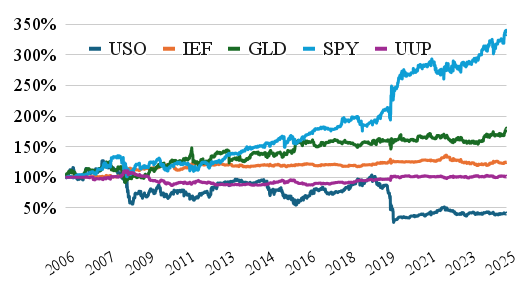

We look at the 5 main asset lessons and use the next ETFs as proxies:

Commodities (represented by oil ETF USO)

Fastened revenue securities (bonds, ETF IEF)

Valuable metals (gold ETF GLD)

Equities (inventory index ETF SPY)

Currencies (bullish US Greenback ETF UUP)

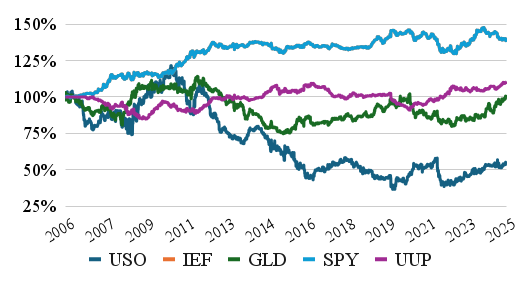

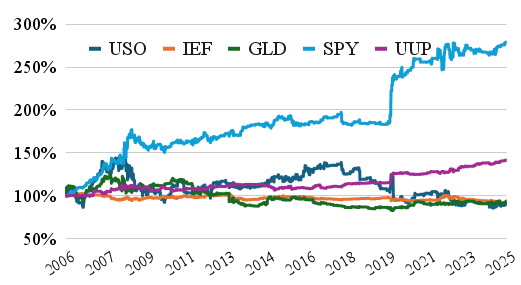

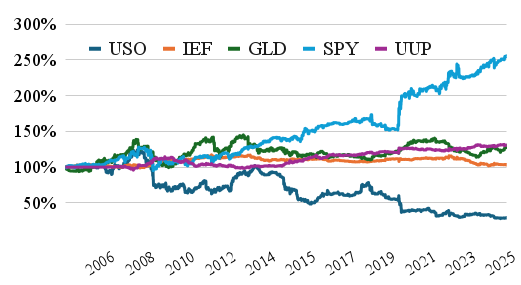

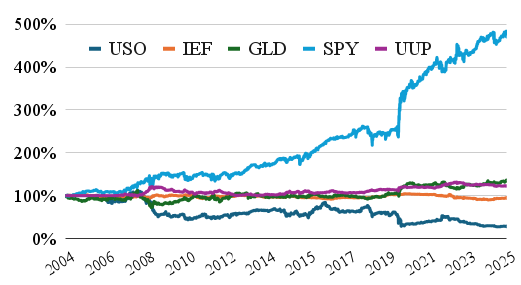

Our information pattern begins in 2004 for SPY, IEF, and GLD, 2006 for USO and UUP, and ends in 2025. For all the ETF historic information, we used information from EODHD.com – the sponsor of our weblog. EODHD affords seamless entry to +30 years of historic costs and elementary information for shares, ETFs, foreign exchange, and cryptocurrencies throughout 60+ exchanges, accessible through API or no-code add-ons for Excel and Google Sheets. As a particular supply, our weblog readers can get pleasure from an unique 30% low cost on premium EODHD plans.

Strategies

We make use of a dynamic threshold mannequin to determine stress occasions, defining them as simultaneous at some point declines in two risk-on asset lessons (SPY-equities, USO-oil, GLD-gold) or at some point decline in a single risk-on asset and appreciation within the risk-off asset (IEF-fixed revenue) past a specified parametric threshold. The mannequin is applied for every devoted pair of asset lessons.

Gold and Equities (2x dangerous property)

Oil and Equities (2x dangerous property)

Oil and Gold (2x dangerous property)

US Treasuries and Gold (1x risk-off and 1x danger on asset)

US Treasuries and Equities (1x risk-off and 1x danger on asset)

US Treasuries and Oil (1x risk-off and 1x danger on asset)

The stress threshold is parameterized, permitting for a versatile definition of stress occasions. As an illustration, a 1% threshold would determine days when each dangerous property in a pair decline by greater than -1% (or one dangerous asset decline greater than -1% and risk-off asset appreciation by greater than +1%). For every mixture, the optimum iteration threshold is reported. 0% optimum threshold signifies that each dangerous property representing particular asset lessons closed negatively on that day (or one dangerous asset declined and, on the similar time, a risk-off asset closed positively).

Easy Buying and selling Technique and Efficiency Analysis

Upon identification of a stress occasion, we implement a one-day buying and selling technique, initiating positions on the shut of the stress day and liquidating on the shut of the following buying and selling day. The evaluation considers 5 potential funding, separately for every of the potential occurrences:

Lengthy oil

Lengthy US treasuries

Lengthy gold

Lengthy equities

Lengthy USD

Efficiency is evaluated utilizing fairness curves for every place sort, accompanied by complete efficiency and danger metrics to be reported in subsequent sections.

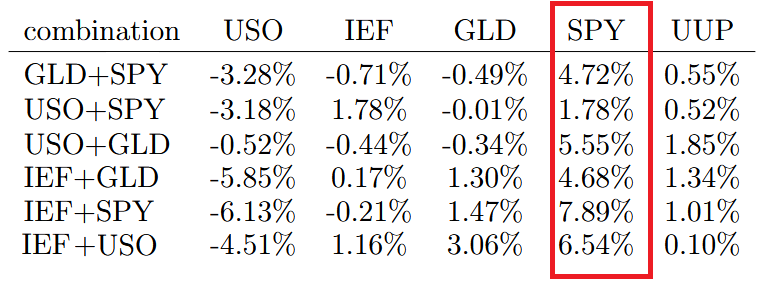

1. Subsequent day response in ETFs after Gold and Equities decline collectively (2x dangerous asset – GLD & SPY decline; 0% threshold)

2. Subsequent day response in ETFs after Oil and Equities decline collectively (2x dangerous asset – USO & SPY decline; 0% threshold)

3. Subsequent day response in ETFs after Oil and Gold decline collectively (2x dangerous asset – USO & GLD decline; -0.5% threshold)

4. Subsequent day response in ETFs after US Treasuries improve and Gold declines (1x danger off asset – IEF & 1x dangerous asset GLD; 0.0% threshold)

5. Subsequent day response in ETFs after US Treasuries improve and Equities decline (1x danger off asset – IEF & 1x dangerous asset SPY; 0.0% threshold)

6. Subsequent day response in ETFs after US Treasuries improve and Oil declines (1x danger off asset – IEF & 1x dangerous asset USO; 0.0% threshold)

Concentrated Property Efficiency for Every Mixture

We will see that fairness markets represented by main S&P 500 index are performing finest after short-term stress, which makes them an excellent asset on which to base correlated reversal methods.

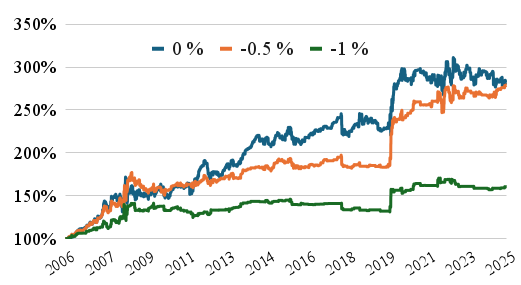

Within the earlier half, we talked about that a number of completely different ranges of threshold can be utilized to sign correlated stress reversal. Right here, we’ll decide one sign pair (USO+GLD mixture), change the brink parameter, and present how the SPY ETF performs if we maintain it at some point after the stress occasion. Different pairs have roughly comparable patterns – the optimum threshold is between 0% and -0.5% transfer for the dangerous asset (or between 0% and +0.5% transfer for the risk-off asset – IEF).

1 Calmar Ratio

Buying and selling Technique with Diversified Indicators

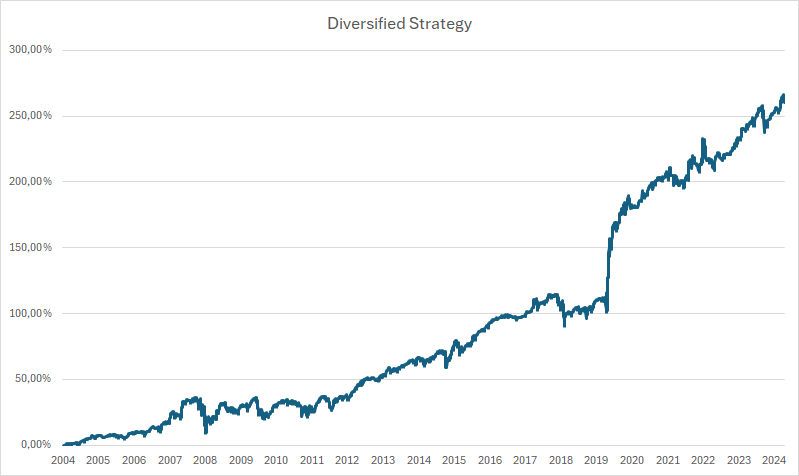

As the very best asset to purchase for the reversal technique is the SPY ETF, and we now have a number of prediction alerts, we will diversify amongst them and construct a composite technique. For example, we will decide the next three predictors:

at some point improve in IEF and simultaneous at some point lower in GLD

at some point improve in IEF and simultaneous at some point lower in USO

at some point improve in IEF and simultaneous at some point lower in SPY

Let’s another time overview the cumulative return fairness curves of this three distinct funding methods:

Subsequently, we conclude the evaluation by presenting a remaining portfolio technique, computing the equally weighted common returns from these three methods, and offering an related efficiency desk for this aggregated technique.

This examine offers worthwhile insights into the habits of main asset lessons during times of correlated stress occasions, the place simultaneous declines happen throughout equities, and commodities, and flight to security exists in fastened revenue. Using a parameterized threshold mannequin, we might flexibly determine stress occasions and analyze subsequent asset class reactions, revealing nuanced, regime-dependent cross-asset dynamics. Our findings spotlight that U.S. equities are likely to carry out finest within the quick time period following these stress episodes, suggesting their potential function as a tactical asset in portfolio rebalancing methods.Moreover, the examine’s consequent buying and selling methods, which mix a number of asset pairs and optimize stress thresholds, demonstrated enhanced risk-adjusted returns. The composite portfolio method, aggregating methods throughout gold, fastened revenue, oil, and equities, underscores the advantages of diversification and tactical asset allocation throughout market stress. These outcomes align with broader literature emphasizing the benefit of offering liquidity and shopping for short-term stress in risky environments.

Creator: Cyril Dujava, Quant Analyst, Quantpedia

Are you searching for extra methods to examine? Join our publication or go to our Weblog or Screener.

Do you wish to be taught extra about Quantpedia Premium service? Test how Quantpedia works, our mission and Premium pricing supply.

Do you wish to be taught extra about Quantpedia Professional service? Test its description, watch movies, overview reporting capabilities and go to our pricing supply.

Are you searching for historic information or backtesting platforms? Test our record of Algo Buying and selling Reductions.

Or observe us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookConsult with a good friend

")