We’ll assume you already know {that a} put credit score unfold has a constructive delta, constructive theta, and damaging vega.

At this time, we are going to dive deep into how these Greeks change with completely different configurations of the put credit score unfold.

Contents

Questions like:

How does shifting a put credit score unfold nearer to the cash have an effect on the delta?

What occurs to theta when the unfold is additional out in time?

What occurs to vega once we improve the unfold width?

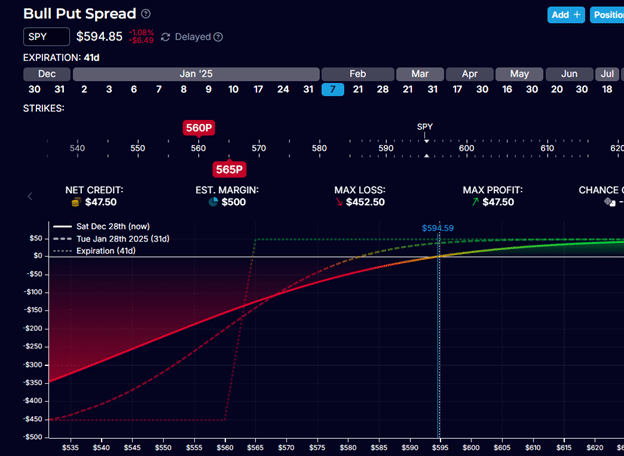

Right here is an out-of-the-money put credit score unfold on SPY that’s 41 days out in time.

Promote one contract Feb 7, 2025, SPY $565 put at $3.09Buy one contract Feb 7, 2025, SPY $560 put at $2.62

Web credit score: $47.50

Max loss: $452.50

Danger-to-reward: 9.5

The delta of the lengthy $560 put possibility is -13, and the delta of the brief $565 put possibility is 16.

Thus, this unfold has its brief possibility on the 16 delta.

A protracted put has a damaging delta as a result of it advantages if the underlying worth goes down.

A brief put has a constructive delta as a result of it advantages if the worth goes up.

After we mix the 2 legs, the Greeks for the bull put credit score unfold on a per contract foundation are:

Delta: 2.7Theta: 0.66Vega: -5.46Gamma: -0.11

The general constructive delta reveals that the unfold has a bullish directionality.

The constructive theta reveals that this unfold advantages from the passage of time.

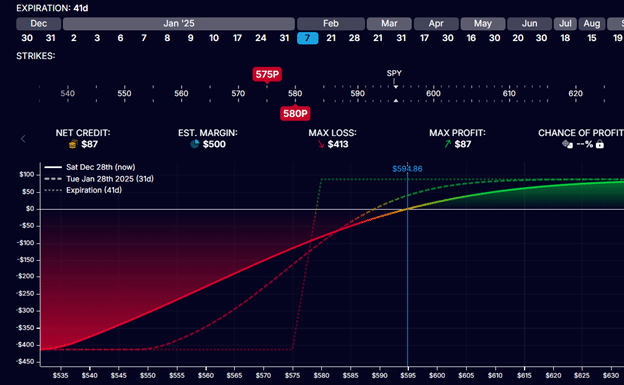

If this identical 5-point-wide unfold was positioned nearer to the cash with the identical expiration, we’ve:

Preliminary credit score: $87

Max Danger: $413

Danger-to-reward: 4.7

A more in-depth to the cash unfold provides a much bigger preliminary credit score.

This is the reason you’re going to get a credit score for this roll while you roll a diffusion nearer to the cash (whereas conserving the unfold width and expiration the identical).

Due to the bigger credit score (with the identical unfold width), we’ve decreased the utmost threat of unfold (from $452.50 to $413).

And thereby decreasing the risk-to-reward ratio.

Let’s have a look at the Greeks.

Delta: 4.70Theta: 0.40Vega: -5.95Gamma: -0.16

Transferring the unfold nearer elevated the directionality of the unfold (bigger delta) and elevated gamma (the speed of change of delta as the worth of SPY strikes).

A diffusion nearer to the cash can have much less time decay, as indicated by a smaller theta.

Free Wheel Technique eBook

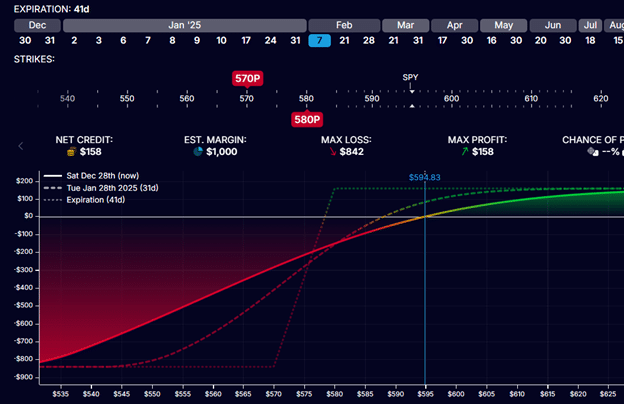

If we have been to widen the width of the credit score unfold to 10 factors, as in:

We’d obtain a bigger credit score for a bigger threat, rising the risk-to-reward barely:

Credit score: $158

Max threat: $842

Danger to reward: 5.3

How did the Greeks change?

Delta: 8.60Theta: 0.93Vega: -11.96Gamma: -0.31

We now have elevated the directionality of the unfold and its gamma much more.

And the magnitude of vega has elevated.

Not less than we’ve now bumped up theta as a result of the lengthy protecting leg of the unfold much less impedes theta.

After we maintain rising the width of the unfold an increasing number of, it begins to behave an increasing number of like a single brief put (nearer to that of an undefined threat place).

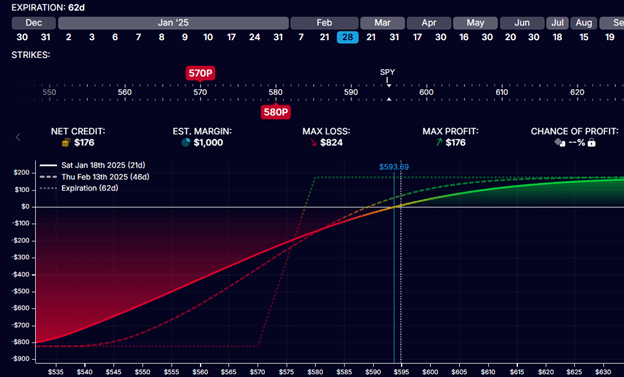

We’ll maintain the identical strikes at $580 and $570 however place the unfold at a later expiration (reminiscent of Feb 28, two weeks later).

We get an excellent bigger credit score as a result of we’re promoting extra extrinsic worth.

Credit score: $176

Max threat: $824

Danger to reward: 4.6

When a credit score unfold shouldn’t be understanding or getting too near expiration, some merchants will prefer to roll the unfold to a later expiration.

This implies closing out the prevailing unfold and opening a brand new unfold with the identical width at a later expiration date.

Ideally, they’ll need to get a credit score for this adjustment.

Which means the preliminary credit score of a brand new unfold must be bigger than it prices to shut the prevailing unfold.

If they’ll get this with out altering the unfold width, they might improve their credit score and thereby scale back their max threat.

The max threat in a credit score unfold is the width of the unfold minus the credit obtained.

Let’s have a look at the Greeks, who’re additional dated and unfold two months out in time.

Delta: 7.91Theta: 0.39Vega: -11.58Gamma: -0.23

The magnitude of each Greek decreases.

The Greeks are much less robust additional out in time.

Figuring out the Greeks of a credit score unfold is necessary in preliminary placement and in adjusting.

A dealer who’s assured available in the market course could place a diffusion nearer to the cash for higher directionality.

A dealer primarily fascinated about accumulating premiums from time decay could need to place the unfold additional away from the cash for the elevated theta.

A dealer who doesn’t have time to test the markets usually could need to place the unfold additional out in time.

As a result of the delta won’t change a lot for the reason that magnitude of gamma is decrease.

When a credit score unfold approaches expiration, gamma will increase.

If this gamma is an excessive amount of, a dealer could roll the unfold out in time to cut back the gamma.

A dealer might also roll the unfold additional out in time if the unfold is being threatened, with the worth coming nearer to the brief strike.

So long as the dealer retains the unfold width the identical and collects a credit score for the roll, this decreases the most threat within the commerce.

It additionally decreases the directionality of the unfold (delta is decrease).

If a dealer trades two out-of-the-money credit score spreads (as in an iron condor), he could roll the un-threatened unfold nearer to the cash to gather further credit.

Do not forget that an out-of-the-money credit score unfold (whether or not put or name spreads) will accumulate further credit score while you roll it nearer to the cash.

This extra credit score offsets the utmost threat of the commerce (so long as the width of the unfold stays the identical).

Sure unfold configurations could also be “higher” for one dealer however not for one more.

Choices are often pretty priced.

So for those who suppose, “Hey, have a look at how rather more credit score I can get for this unfold over the opposite one.”

You have to ask what you take on or giving as much as get this credit score.

In case you transfer your unfold nearer to the cash, sure, you get extra credit score, however you take on extra directional threat.

In case you transfer your unfold additional out in time, you get extra credit score, however you now have much less theta.

In case you suppose attempting to get the biggest theta is the “finest,” suppose once more.

Sure, you may get extra theta by shifting the unfold nearer to expiration, however now you take on directional threat (bigger delta) and gamma threat (bigger magnitude of gamma).

You may then say, “Properly, I’ll transfer my unfold far out of the cash.”

Then I’ve low delta and low gamma however nonetheless considerably excessive theta.

Sure, that configuration focuses on capturing earnings from time decay.

Nonetheless, its risk-to-reward ratio is inferior to the opposite configurations.

We hope you loved this text on the choices Greeks of a put credit score unfold.

In case you have any questions, please ship an e mail or depart a remark beneath.

Commerce secure!

Disclaimer: The data above is for instructional functions solely and shouldn’t be handled as funding recommendation. The technique introduced wouldn’t be appropriate for buyers who usually are not aware of change traded choices. Any readers on this technique ought to do their very own analysis and search recommendation from a licensed monetary adviser.

")