Entrance Working in Nation ETFs, or Tips on how to Spot and Leverage Seasonality

Understanding seasonality in monetary markets requires recognizing how predictable return patterns might be influenced by investor conduct. One underexplored facet of that is the impression of front-running—the place merchants anticipate seasonal developments and act early, shifting returns ahead in time. We now have already explored seasonality front-running in commodities, inventory sectors, and disaster hedge portfolios. Our new analysis examines whether or not this phenomenon extends to nation ETFs, an asset class the place seasonality has been much less studied. By making use of a front-running technique to a dataset of nation ETFs, we establish alternatives to capitalize on seasonal results earlier than they absolutely materialize. Our findings point out that pre-seasonality drift is strongest in commodities however stays current in nation ETFs, providing a possible edge in portfolio development. In the end, our research highlights how front-running seasonality can improve ETF investing, offering a further layer of market timing past conventional trend-following approaches.

Introduction

Seasonality is a well-documented phenomenon in monetary markets, the place sure belongings exhibit recurring patterns in returns based mostly on time-based components reminiscent of months, quarters, or financial cycles. It generally seems in commodity markets (Dealer’s Information to Entrance-Working Commodity Seasonality), inventory sectors (Entrance-Working Seasonality in US Inventory Sectors) or disaster hedge portfolios (Seasonality Patterns within the Disaster Hedge Portfolios).

As soon as tradable belongings change into accessible, they’re topic to entrance working—traders anticipating seasonal developments start accumulating positions earlier than the anticipated seasonality manifests. This entrance working impact can create worth drifts, shifting returns ahead in time and doubtlessly diminishing or reshaping the unique seasonal sample. Whereas not all belongings expertise this impact, it’s removed from uncommon. Understanding these dynamics might help traders establish when and the place seasonality is being priced in early, providing alternatives to capitalize on market inefficiencies.

On this research, we examine whether or not this phenomenon extends to a different section of the market—market ETFs. We study the conduct of those ETFs with a deal with seasonality and, following the strategy of the beforehand talked about research, goal to assemble a front-running technique that successfully leverages seasonal patterns.

Information

On this evaluation, our dataset include month-to-month information from 23 nation ETFs, particularly: SPY – SPDR S&P 500 ETF Belief, EWU – iShares MSCI United Kingdom ETF, EWG – iShares MSCI Germany ETF, EWQ – iShares MSCI France ETF, EWI – iShares MSCI Italy ETF, EWD – iShares MSCI Sweden ETF, EWN – iShares MSCI Netherlands ETF, EWP – iShares MSCI Spain ETF, EWK – iShares MSCI Belgium ETF, EWL – iShares MSCI Switzerland ETF, EWC – iShares MSCI Canada ETF, EWJ – iShares MSCI Japan ETF, EWW – iShares MSCI Mexico ETF, EWM – iShares MSCI Malaysia ETF, EWA – iShares MSCI Australia ETF, EWS – iShares MSCI Singapore ETF, EWY – iShares MSCI South Korea ETF, EWT – iShares MSCI Taiwan ETF, EWZ – iShares MSCI Brazil ETF, EWH – iShares MSCI Hong Kong ETF, EZA – iShares MSCI South Africa ETF, FXI – iShares China Giant-Cap ETF, and INDY – iShares India 50 ETF.

Most of those ETFs had been launched in 1996, the second largest group in 2000; due to this fact, after the yr 2000, we now have historic information for almost all ETFs. Solely EZA, FXI, and INDY had been launched later, in 2003, 2004, and 2009, respectively. To maximise the size of our analysis interval, we didn’t wait till 2009. As an alternative, we used the yr 2000 as the start line for our evaluation, and the final 3 ETFs had been included progressively after their inception. In different phrases, we tried to make a trade-off between information availability and the variety of ETFs within the preliminary portfolio. The latest information used was from February 2025.

Month-to-month efficiency information had been utilized in all calculations. Fundamental efficiency traits in tables are offered as follows: the notation perf represents the annual return of the technique, st dev stands for the annual customary deviation, max dd is the utmost drawdown, adusted Sharpe Ratio is calculated because the ratio of perf to st dev and adjusted Calmar Ratio because the ratio of perf to max dd.

Methodology

As talked about within the first paragraph, this research focuses on seasonality, which we goal to leverage in making a worthwhile technique. Given the supply of tradable belongings, we imagine front-running is an acceptable strategy. The process is simple – if we’re assured that an asset performs nicely in a selected month, shopping for it one month earlier, earlier than most traders do, might be more practical, as their later purchases drive the value increased.

And now, we are able to transfer on to the technique itself. On the finish of every month, we utilized a cross-sectional strategy to seasonality, rating the efficiency of all included ETFs based mostly on their returns from the month T-11 (e.g., on the finish of March, investments for April had been ranked based mostly on their efficiency in Could of the earlier yr). This rating was carried out relative to the opposite ETFs within the choice. Primarily based on these rankings, we invested in a particular variety of top-performing ETFs for the next month.

However what number of ETFs ought to we embody in our portfolio? We determined to depend on acquired information, and for robustness functions, we included all important picks. Due to this fact, we examined a number of thresholds: vigintile (prime 5%), decile (prime 10%), quintile (prime 20%), quartile (prime 25%), tercile (prime 33%), and half (50%). This implies we utilized the front-running technique to the highest 1 to 11 ranked investments.

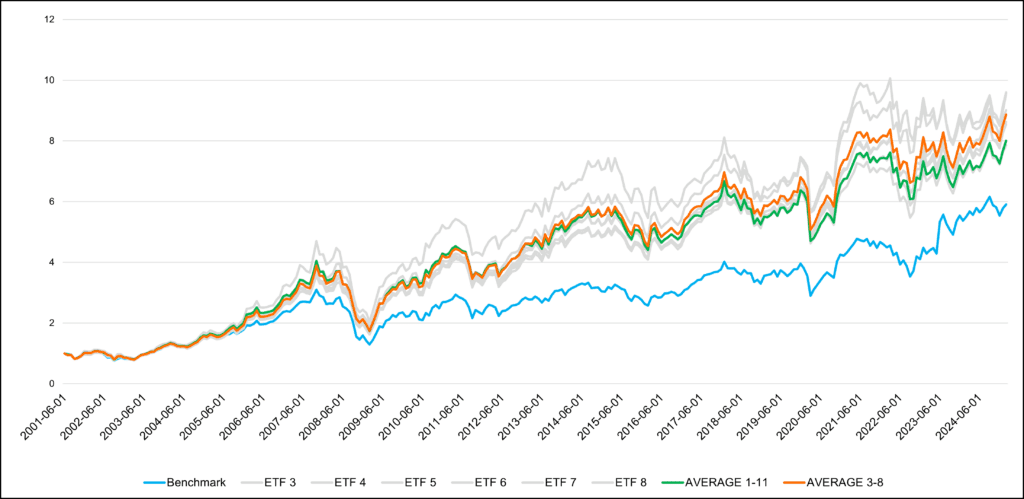

Within the subsequent step, we constructed a benchmark – an equally weighted common of all 23 ETFs. Moreover, we included an equally weighted common of the 11 front-running methods, deciding on the highest 1 to 11 ETFs with the very best efficiency within the front-running months. Now, we’re lastly able to assess the profitability of our technique.

As we are able to see within the graph in Determine 1, for nearly the complete interval, almost all front-running methods and their common outperformed the benchmark. There’s one exception: the front-running technique, which selects just one ETF, which has skilled a major downturn since 2019. All different methods, and thus the common 1-11, simply outperformed the benchmark.

Nonetheless, methods positioned in the midst of our examined pattern achieved probably the most favorable outcomes. Plainly it’s not a good suggestion to be too concentrated (choosing simply the 1 or 2 ETFs). It’s additionally not a good suggestion to be overly diversified (because the front-running sign is then too diluted amongst too many ETFs). The candy spot is to select between 3-8 ETFs (so the highest quintile, quartile, or tercile of ETFs based mostly on the front-running seasonality sign). So, within the subsequent step, we retained solely the methods based mostly on the highest 3 to prime 8 ETFs and averaged them out to construct a remaining front-running technique. Let’s assess whether or not we made the appropriate determination.

As anticipated, the shortened choice simply outperformed not solely the benchmark but additionally the broader common. Due to this fact, we advocate adopting the common of shortened choice as the ultimate technique, much like our strategy within the research Can Margin Debt Assist Predict SPY’s Progress & Bear Markets?. We think about the marginally increased outcomes of some methods to have low credibility and to be unlikely to persist in the long term. As a result of imply reversion impact, we favor diversifying our bets throughout all methods to keep up a extra steady mannequin. The ultimate determination, in fact, stays with the reader.

Conclusion

The energy of the pre-seasonality drift is dependent upon the underlying belongings. We observe that it’s strongest in commodities, the place we first recognized it. Whereas the impact is current in different asset lessons, it’s weaker because of the dominance of different basic components. For instance, in equities, the general sturdy constructive drift performs a serious position, as shares are inclined to rise on common, whereas commodities don’t exhibit the identical long-term upward development. Regardless of this, we now have discovered a option to improve funding methods in nation ETFs by implementing an strategy that evenly allocates capital throughout six front-running methods, deciding on 3 to eight ETFs based mostly on the front-running seasonality sign every month. This demonstrates that the front-running seasonality idea stays relevant past commodities.

Creator: Sona Beluska, Junior Quant Analyst, Quantpedia

Are you in search of extra methods to examine? Join our e-newsletter or go to our Weblog or Screener.

Do you need to be taught extra about Quantpedia Premium service? Test how Quantpedia works, our mission and Premium pricing supply.

Do you need to be taught extra about Quantpedia Professional service? Test its description, watch movies, evaluation reporting capabilities and go to our pricing supply.

Are you in search of historic information or backtesting platforms? Test our listing of Algo Buying and selling Reductions.

Or observe us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookCheck with a pal

")