Risks of Counting on OHLC Costs – the Case of In a single day Drift in GDX ETF

Can we actually depend on the opening worth in OHLC knowledge for backtesting? Whereas the in a single day drift impact is well-documented in a variety of asset courses, we investigated its presence in gold utilizing the GLD ETF after which prolonged our evaluation to the GDX – Gold Miners ETF, the place we noticed an unusually sturdy in a single day return exceeding 30% annualized. Nonetheless, once we examined execution at 9:31 AM utilizing 1-minute knowledge, the anomaly diminished considerably, suggesting that the intense return was partially a knowledge artifact. This discovering highlights the dangers of blindly trusting OHLC open costs and underscores the necessity for higher-frequency knowledge to validate execution assumptions.

Background

The in a single day impact and drift in quantitative finance check with the phenomenon the place inventory returns throughout non-trading hours, notably in a single day, exhibit important patterns that differ from these noticed throughout buying and selling hours. The in a single day impact refers back to the tendency of inventory returns to exhibit substantial actions throughout the night time, usually influenced by market dynamics and investor sentiment.

One of many newer papers on this area is “The Cross-Part of Intraday and In a single day Returns” by Vincent Bogousslavsky (2021). This influential work investigates the patterns of intraday and in a single day returns and their implications for asset pricing fashions, offering priceless insights into the habits of monetary markets throughout non-trading hours.

The paper “In a single day Drift” by Boyarchenko, Larsen, and Whelan (2023) additionally explores this attention-grabbing impact. The primary discovering is that U.S. fairness returns are notably constructive throughout the opening hours of European markets, pushed by order imbalances from the earlier buying and selling day. Market sell-offs result in sturdy in a single day reversals, whereas rallies end in modest reversals, indicating an uneven response to demand shocks.

We at Quantpedia explored this impact considerably, too, and found an in a single day impact on Bitcoin returns and high-yield ETF returns. By constructing on this papers we purpose to increase the understanding of in a single day methods and worth drifts, providing new views and leveraging the established SPY drift paradigm and increasing it to the commodities asset class that gold (and gold mining shares) ETFs symbolize.

Knowledge

We initially sourced our knowledge from finance.yahoo.com, making vital changes for dividends. We examined the close-to-open and open-to-close worth actions, which gave us a transparent view of the in a single day and intraday drifts.

Gold ETF

As talked about earlier, we analyzed GLD’s in a single day, intraday, and whole efficiency utilizing historic knowledge from Yahoo Finance. Our evaluation reveals that a good portion of GLD’s efficiency happens in a single day. The GLD ETF’s intraday efficiency during the last 20 years is negligible. These findings are according to the worth motion taking place within the different asset courses we talked about earlier than (particular person shares, fairness indices, cryptocurrencies, or high-yield ETFs).

Nonetheless, as gold is a commodity, there exist firms specializing within the means of extracting this gold from the Earth’s crust (sure, we’re talking about gold miners). Subsequently, we are able to bridge fairness and commodity markets, by shopping for ETFs which put money into such shares, like GDX (VanEck Gold Miners ETF). In concept, this convergent asset ought to give us the potential for mixed in a single day drift results and better earnings, proper?

Let’s discover that.

Gold Miners ETF

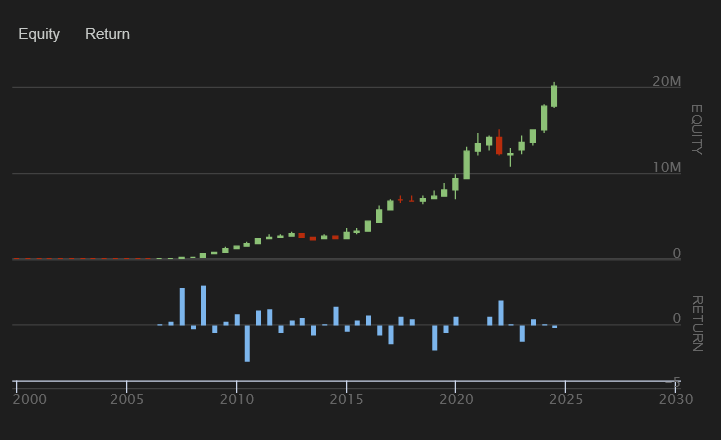

Following the identical method, we carried out the identical process utilizing GDX OHLC (open, excessive, low, shut) knowledge. Our evaluation reveals a big in a single day drift of roughly 30% every year (p.a.), contrasted by a considerable unfavorable intraday drift of about -25% every year. These findings immediate a logical buying and selling technique: iteratively buying at market open and shorting at market shut. Theoretically, this method may yield important returns over time.

Wow, we may get wealthy fast right here! Or not? Properly, truly, from the expertise, this seems to be to good to be true. We have to examine the underlying drawback.

From our expertise, the issue is normally hidden within the opening costs of the OHLC datasets. Notably, the opening worth is derived from the primary commerce moderately than the MOO (Market-on-Open) public sale outcomes, resulting in important discrepancies between anticipated and precise opening costs as one is unable to even carefully method getting fills in that worth area, not talking about volumes traded at that costs which have to be minuscule. That is widespread drawback when utilizing the OHLC knowledge. The shut costs are normally achievable in actuality by buying and selling (shopping for/promoting) near the top of the buying and selling session or collaborating within the closing public sale by way of MOC (Market-on-Shut) orders. Traditionally, closing costs on monetary platforms reminiscent of Yahoo Finance normally align with MOC public sale costs.

Whereas executing on the shut sometimes presents no points for opening costs, the fact is usually very totally different. Subsequently, our ordinary subsequent step is at all times to revert to testing anomalies and results with higher knowledge granularity (minute-by-minute bars, second-by-second bars, or tick knowledge). Subsequently, let’s attempt to modify the execution of the promote sign from 9:30 AM to 9:31 AM. One minute shouldn’t make a distinction, proper? For that, we transitioned to the QuantConnect setting as intraday TOC (Time-of-Change) knowledge are vital.

SPY and GDX In a single day Results Analysis

Let’s transfer to judge the efficiency of in a single day buying and selling methods utilizing

SPDR S&P 500 ETF (SPY) and

VanEck Vectors Gold Miners ETF (GDX).

It focuses on execution timing, specifically

Market-on-Open (MOO), vs.

a selected intraday execution at 9:31 AM.

Numerous Situations

SPY Buying and selling Technique:

Situation 1: SPY, purchase MOC, promote MOO.

Situation 2: SPY, purchase MOC, promote 9:31.

GDX Buying and selling Technique:

Situation 1: GDX, purchase MOC, promote MOO.

Situation 2: GDX, purchase MOC, promote 9:31.

SPY

Situation 1

Situation 2

Our backtest outcomes present solely slight variations between executing on the open worth and the precise intraday time of 9:31 AM, with the latter exhibiting rather less revenue. The in a single day impact is properly and alive. Sure, there’s a slight lower in efficiency for those who execute a promote order at 9:31 AM (in comparison with the hypothetical execution at 9:30), however the lower is small, and the impact continues to be current as a big a part of the SPY whole return during the last years is registered over the night time session, and it doesn’t matter rather a lot if that night time session ends at 9.30 or 9.31.

GDX

Situation 1

Backtest outcomes exhibit extremely unrealistic, excessive numbers.

Situation 2

However, our backtests on the GDX ETF can’t be extra totally different. The backtest utilizing the OHLC knowledge additionally exhibits completely unrealistic efficiency, roughly 30% every year, for the in a single day drift technique. However, the second state of affairs, wherein the promote sign is executed at 9:31 AM, yields a considerably extra real looking end result. The efficiency of the GDX in a single day technique (earlier than charges and slippage) is 8,58% every year, with a -40,7% most drawdown and 16.9% volatility. Sure, the in a single day drift in GDX costs is unquestionably there, too. Nonetheless, the magnitude of the impact is just not as excessive because the evaluation utilizing the OHLC knowledge hinted.

Dialogue & Conclusion

The in a single day drift signifies a notable sample the place a lot of the asset’s efficiency is pushed by in a single day actions. This discovering aligns with our observations in different asset courses, suggesting a broader applicability of in a single day drift phenomena. Along with elucidating the in a single day drift in conventional asset courses reminiscent of equities, our investigation underscores the crucial significance of sturdy methodological scrutiny in backtesting buying and selling methods. Particularly, the pronounced discrepancies noticed between theoretically derived and virtually executable costs spotlight potential pitfalls within the naive utility of OHLC knowledge.

The discrepancy in backtest efficiency for GDX is attributed to the methodology used to report open costs (open costs) in OHLC knowledge. It’s impractical to count on execution on the reported open costs. Subsequently, rigorous consideration needs to be paid when growing methods that presume execution at open costs. It’s advisable to conduct robustness assessments and confirm efficiency with intraday execution costs, reminiscent of these at 9:31 AM, to make sure extra dependable outcomes.

Creator: Cyril Dujava, Quant Analyst, Quantpedia

Are you searching for extra methods to examine? Join our publication or go to our Weblog or Screener.

Do you need to be taught extra about Quantpedia Premium service? Examine how Quantpedia works, our mission and Premium pricing provide.

Do you need to be taught extra about Quantpedia Professional service? Examine its description, watch movies, evaluation reporting capabilities and go to our pricing provide.

Are you searching for historic knowledge or backtesting platforms? Examine our listing of Algo Buying and selling Reductions.

Or observe us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookCheck with a pal