Revealed on July twenty fourth, 2025 by Bob Ciura

The S&P 500 Index is buying and selling at valuations not seen for the reason that tech bubble of 1999-2000, in line with the Shiller P/E ratio.

The Shiller P/E ratio relies on common inflation-adjusted earnings from the earlier 10 years, often known as the Cyclically Adjusted PE Ratio.

This smooths out fluctuations in earnings on a year-to-year foundation.

The historic imply Shiller P/E ratio is 17.3. It’s presently at 38.8. Due to this fact, the S&P 500 is ~124% overvalued in line with the Shiller P/E ratio.

When the market is overvalued, buyers ought to look to high-quality dividend shares to cut back portfolio volatility, to offer rising earnings annually which might help offset declining share costs.

With this in thoughts, we created a listing of over 500 blue chip shares, which have every raised their dividends for no less than 10 consecutive years.

You possibly can obtain our full blue chip shares listing by clicking on the hyperlink under:

There are presently greater than 500 securities in our blue chip shares listing.

Shopping for overvalued shares can result in low (and even unfavourable) whole returns, even together with dividends.

Due to this fact, buyers must be cautious relating to overvalued dividend shares. The next 10 dividend shares are overvalued in contrast with the imply Shiller P/E of the inventory market.

The listing is sorted by the P/E ratio, in ascending order.

Desk of Contents

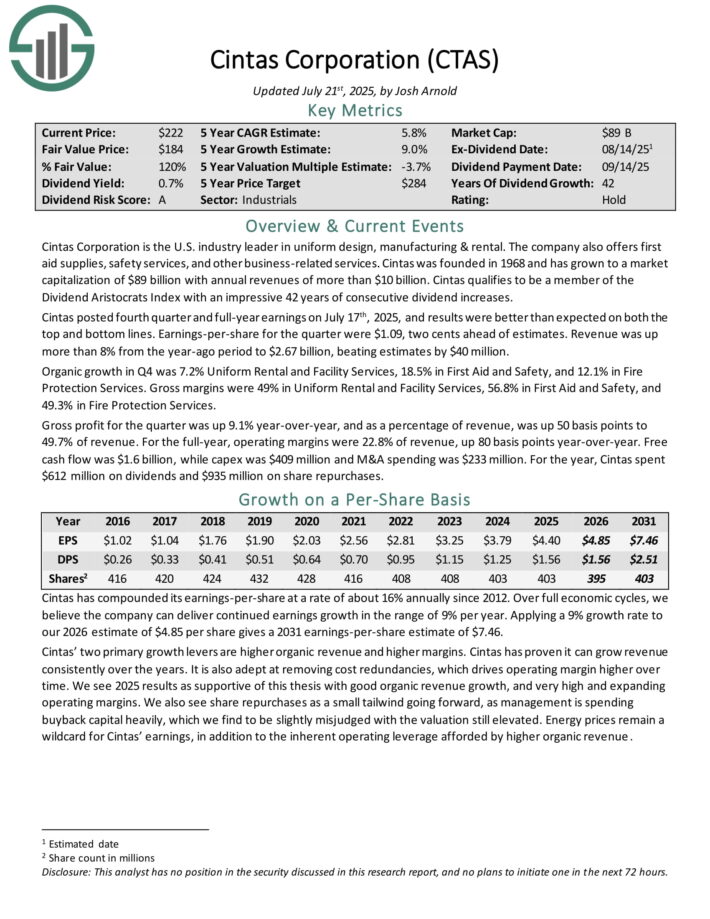

Excessive P/E Inventory #10: Cintas Company (CTAS)

Cintas Company is the U.S. business chief in uniform design, manufacturing & rental. The corporate additionally affords first help provides, security providers, and different business-related providers. Cintas was based in 1968 and now generates annual revenues of greater than $10 billion.

Cintas posted fourth quarter and full-year earnings on July seventeenth, 2025, and outcomes had been higher than anticipated on each the highest and backside strains. Earnings-per-share for the quarter had been $1.09, two cents forward of estimates. Income was up greater than 8% from the year-ago interval to $2.67 billion, beating estimates by $40 million.

Natural progress in This fall was 7.2% Uniform Rental and Facility Companies, 18.5% in First Support and Security, and 12.1% in Fireplace Safety Companies. Gross margins had been 49% in Uniform Rental and Facility Companies, 56.8% in First Support and Security, and 49.3% in Fireplace Safety Companies.

Gross revenue for the quarter was up 9.1% year-over-year, and as a share of income, was up 50 foundation factors to 49.7% of income. For the full-year, working margins had been 22.8% of income, up 80 foundation factors year-over-year. Free money circulate was $1.6 billion, whereas capex was $409 million and M&A spending was $233 million.

Click on right here to obtain our most up-to-date Positive Evaluation report on CTAS (preview of web page 1 of three proven under):

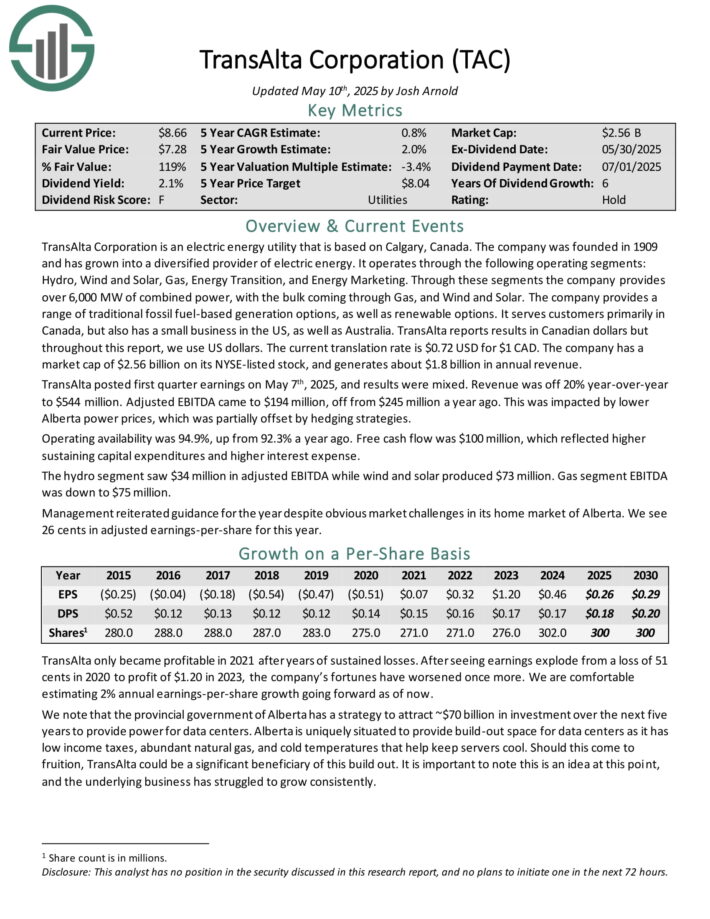

Excessive P/E Inventory #9: TransAlta Company (TAC)

TransAlta Company is an electrical vitality utility that’s based mostly on Calgary, Canada. The corporate was based in 1909 and has grown right into a diversified supplier of electrical vitality. It operates by means of the next working segments: Hydro, Wind and Photo voltaic, Fuel, Power Transition, and Power Advertising.

By means of these segments the corporate gives over 6,000 MW of mixed energy, with the majority coming by means of Fuel, and Wind and Photo voltaic.

The corporate gives a variety of conventional fossil fuel-based era choices, in addition to renewable choices. It serves clients primarily in Canada, but in addition has a small enterprise within the US, in addition to Australia.

TransAlta reviews leads to Canadian {dollars} however all through this report, we use US {dollars}. The present translation charge is $0.72 USD for $1 CAD.

TransAlta posted first quarter earnings on Might seventh, 2025, and outcomes had been blended. Income was off 20% year-over-year to $544 million. Adjusted EBITDA got here to $194 million, off from $245 million a yr in the past. This was impacted by decrease Alberta energy costs, which was partially offset by hedging methods.

Working availability was 94.9%, up from 92.3% a yr in the past. Free money circulate was $100 million, which mirrored larger sustaining capital expenditures and better curiosity expense.

Click on right here to obtain our most up-to-date Positive Evaluation report on TAC (preview of web page 1 of three proven under):

Excessive P/E Inventory #8: Ferrari N.V. (RACE)

Ferrari was based in 1947 and is headquartered in Italy. The corporate started buying and selling as a public firm in 2015, following a derivative from Fiat Chrysler. Right this moment, the corporate manufactures luxurious sports activities vehicles underneath a wide range of fashions.

Its vehicles are typically excessive efficiency, with quite a lot of V-8 and V-12 fashions amongst its greatest sellers. Ferrari’s luxurious autos cater to the very high of the patron automotive market. In 2020, shipments fell greater than 10% to 9,119 items, with about half of that in Europe, Center East, and Africa, and a 3rd coming from the Americas.

On February twentieth, 2025, Ferrari raised its annual dividend 30.3% to $3.39, which follows the corporate’s 30.2% and 35.8% will increase during the last two years. Ferrari has now raised its dividend 4 consecutive years in USD.

On Might sixth, 2025, Ferrari reported first quarter outcomes for the interval ending March thirty first, 2025. All figures reported in USD. For the quarter, income grew 19.5% to $2.04 billion, which beat estimates by $18 million.

Earnings-per-share of $2.62 in contrast favorably to earnings-per-share of $2.10 within the prior yr, which was $0.08 greater than anticipated.

For the quarter, items shipped totaled 3,593, which represented a 0.9% enhance from Q1 2024. Shipments grew 25 items for the Americas and 128 items for the EMEA.

Unit shipments declined 80 for Mainland China, Hong Kong, and Taiwan and had been decrease by 40 items for the Remainder of Asia.

Click on right here to obtain our most up-to-date Positive Evaluation report on RACE (preview of web page 1 of three proven under):

Excessive P/E Inventory #7: Rollins, Inc. (ROL)

Rollins gives pest management and wildlife safety providers. Its merchandise defend rodents, termite harm, and different bugs. The corporate owns a number of main manufacturers and gives providers and merchandise to over two million residential and business clients in over 70 international locations.

Rollins operates underneath one reportable phase and has three enterprise segments: Residential, Business, and Termite. The US is Rollins’s most important geographic location, because it generates over 90% of its income.

On April twenty third, 2025, Rollins introduced outcomes for Q1 2025, reporting normalized EPS of $0.22 in-line analysts’ estimates. The corporate reported revenues of $822.5 million for the quarter, which had been up 10.0% year-over-year.

For the primary quarter of 2025, the pest management and shopper providers big reported revenues of $823 million, up practically 10% from final yr, with natural income climbing 7.4% regardless of foreign money headwinds.

Adjusted EBITDA was strong too, up virtually 7% at $172 million. Working money circulate stood out, leaping 15.3% to $147 million, a testomony to the corporate’s give attention to wholesome margins and disciplined investments.

Click on right here to obtain our most up-to-date Positive Evaluation report on ROL (preview of web page 1 of three proven under):

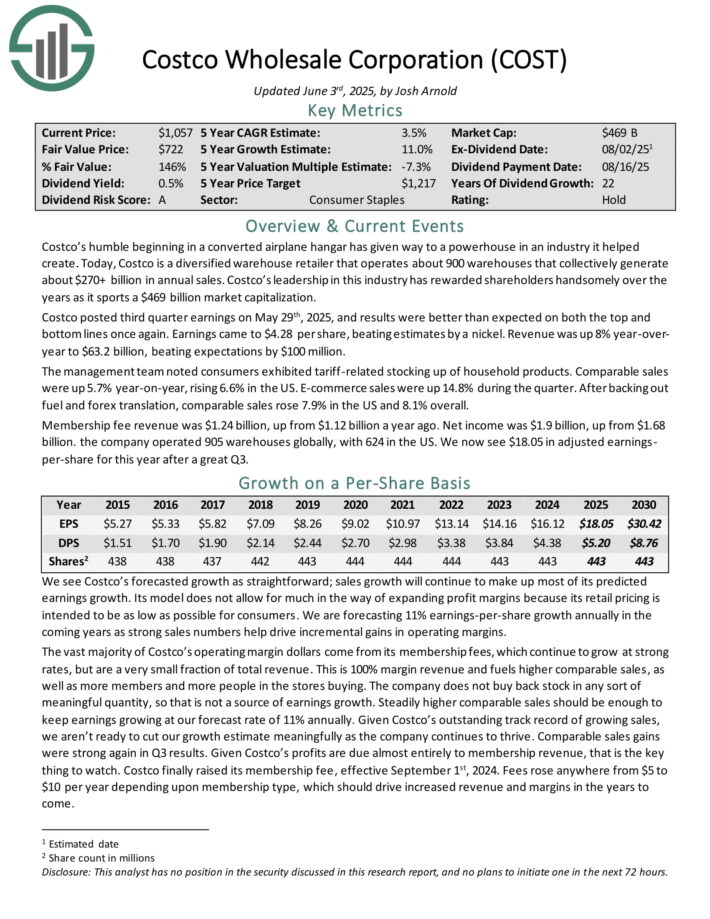

Excessive P/E Inventory #6: Costco Wholesale Corp. (COST)

Costco is a diversified warehouse retailer that operates about 900 warehouses that collectively generate about $270+ billion in annual gross sales.

Costco posted third quarter earnings on Might twenty ninth, 2025, and outcomes had been higher than anticipated on each the highest and backside strains as soon as once more. Earnings got here to $4.28 per share, beating estimates by a nickel. Income was up 8% year-over-year to $63.2 billion, beating expectations by $100 million.

The administration workforce famous customers exhibited tariff-related stocking up of family merchandise. Comparable gross sales had been up 5.7% year-on-year, rising 6.6% within the US. E-commerce gross sales had been up 14.8% throughout the quarter. After backing out gas and foreign exchange translation, comparable gross sales rose 7.9% within the US and eight.1% total.

Membership payment income was $1.24 billion, up from $1.12 billion a yr in the past. Internet earnings was $1.9 billion, up from $1.68 billion. the corporate operated 905 warehouses globally, with 624 within the US.

Click on right here to obtain our most up-to-date Positive Evaluation report on COST (preview of web page 1 of three proven under):

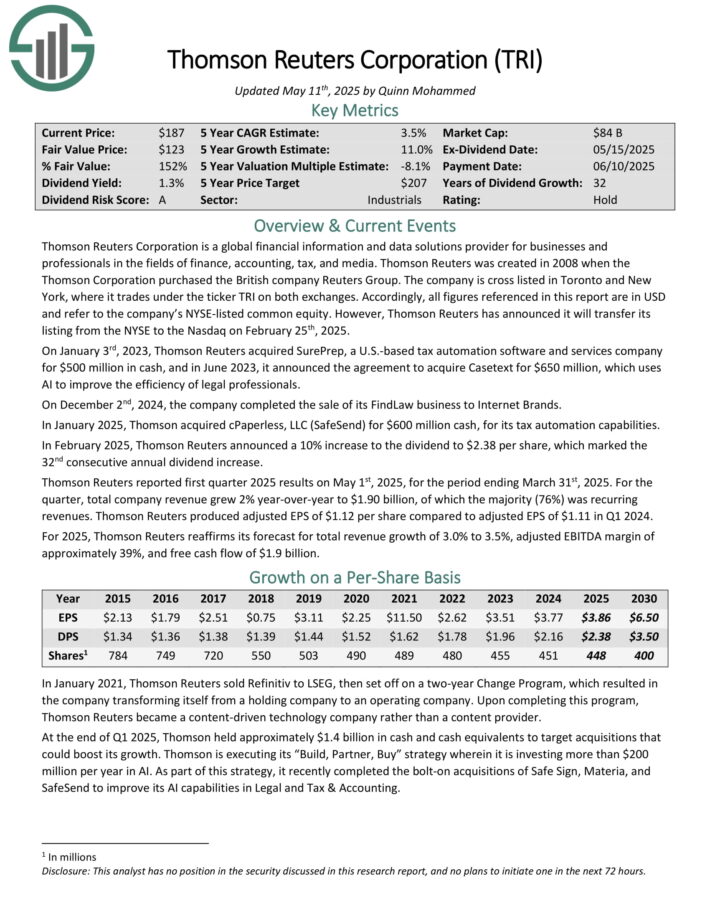

Excessive P/E Inventory #5: Thomson-Reuters Corp. (TRI)

Thomson Reuters Company is a worldwide monetary data and information options supplier for companies and professionals within the fields of finance, accounting, tax, and media.

Thomson Reuters was created in 2008 when the Thomson Company bought the British firm Reuters Group.AI to enhance the effectivity of authorized professionals.

In January 2025, Thomson acquired cPaperless, LLC (SafeSend) for $600 million money, for its tax automation capabilities.

In February 2025, Thomson Reuters introduced a ten% enhance to the dividend to $2.38 per share, which marked the thirty second consecutive annual dividend enhance.

Thomson Reuters reported first quarter 2025 outcomes on Might 1st, 2025, for the interval ending March thirty first, 2025. For the quarter, whole firm income grew 2% year-over-year to $1.90 billion, of which the bulk (76%) was recurring revenues.

Thomson Reuters produced adjusted EPS of $1.12 per share in comparison with adjusted EPS of $1.11 in Q1 2024.

Click on right here to obtain our most up-to-date Positive Evaluation report on TRI (preview of web page 1 of three proven under):

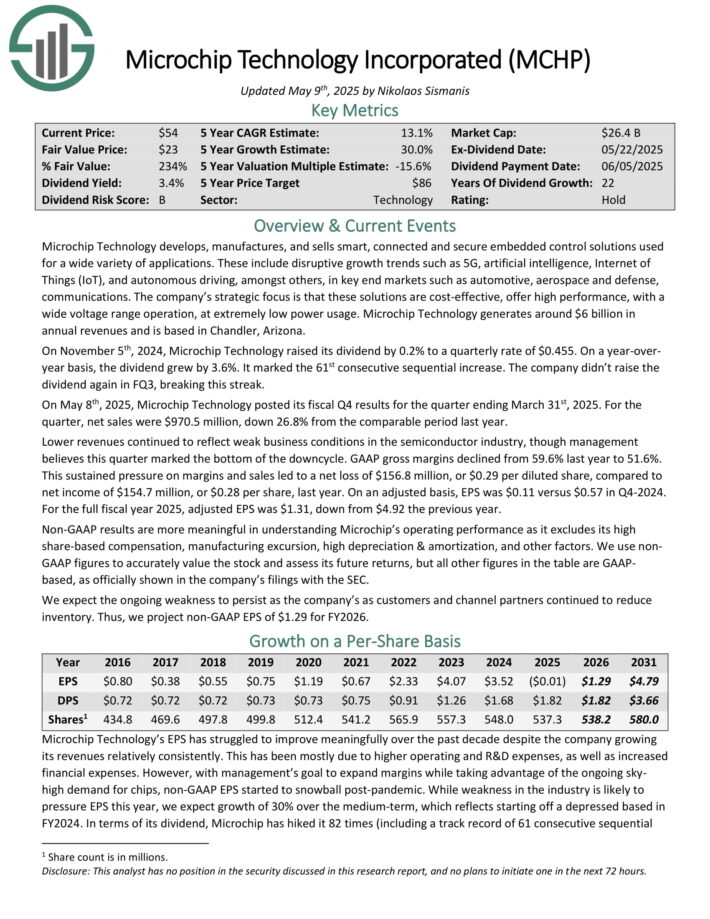

Overvalued Dividend Inventory #4: Microchip Expertise (MCHP)

Microchip Expertise develops, manufactures, and sells sensible, linked and safe embedded management options used for all kinds of functions.

These embrace disruptive progress traits comparable to 5G, synthetic intelligence, Web of Issues (IoT), and autonomous driving, amongst others, in key finish markets comparable to automotive, aerospace and protection, communications.

Microchip Expertise generates round $6 billion in annual revenues and relies in Chandler, Arizona.

On Might eighth, 2025, Microchip Expertise posted its fiscal This fall outcomes for the quarter ending March thirty first, 2025. For the quarter, web gross sales had been $970.5 million, down 26.8% from the comparable interval final yr.

Decrease revenues continued to replicate weak enterprise circumstances within the semiconductor business, although administration believes this quarter marked the underside of the downcycle. GAAP gross margins declined from 59.6% final yr to 51.6%.

This sustained stress on margins and gross sales led to a web lack of $156.8 million, or $0.29 per diluted share, in comparison with web earnings of $154.7 million, or $0.28 per share, final yr. On an adjusted foundation, EPS was $0.11 versus $0.57 in This fall-2024.

Click on right here to obtain our most up-to-date Positive Evaluation report on MCHP (preview of web page 1 of three proven under):

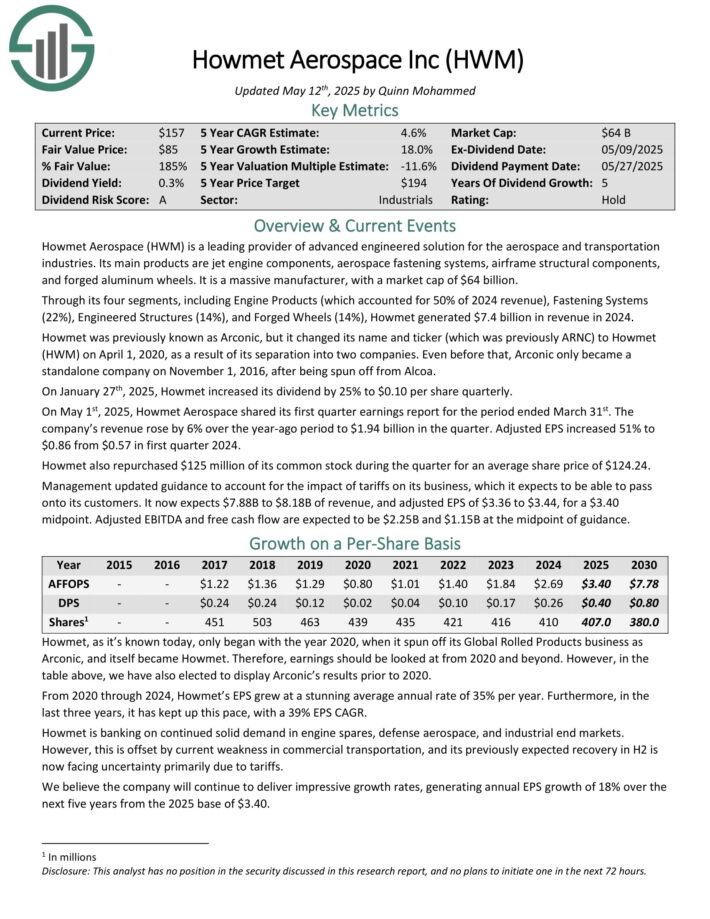

Excessive P/E Inventory #3: Howmet Aerospace (HWM)

Howmet Aerospace (HWM) is a number one supplier of superior engineered resolution for the aerospace and transportation industries. Its most important merchandise are jet engine parts, aerospace fastening methods, air body structural parts, and solid aluminum wheels.

By means of its 4 segments, together with Engine Merchandise (which accounted for 50% of 2024 income), Fastening Techniques (22%), Engineered Buildings (14%), and Cast Wheels (14%), Howmet generated $7.4 billion in income in 2024.

On January twenty seventh, 2025, Howmet elevated its dividend by 25% to $0.10 per share quarterly.

On Might 1st, 2025, Howmet Aerospace shared its first quarter earnings report for the interval ended March thirty first. The corporate’s income rose by 6% over the year-ago interval to $1.94 billion within the quarter. Adjusted EPS elevated 51% to $0.86 from $0.57 in first quarter 2024.

Howmet additionally repurchased $125 million of its frequent inventory throughout the quarter for a median share worth of $124.24.

Click on right here to obtain our most up-to-date Positive Evaluation report on HWM (preview of web page 1 of three proven under):

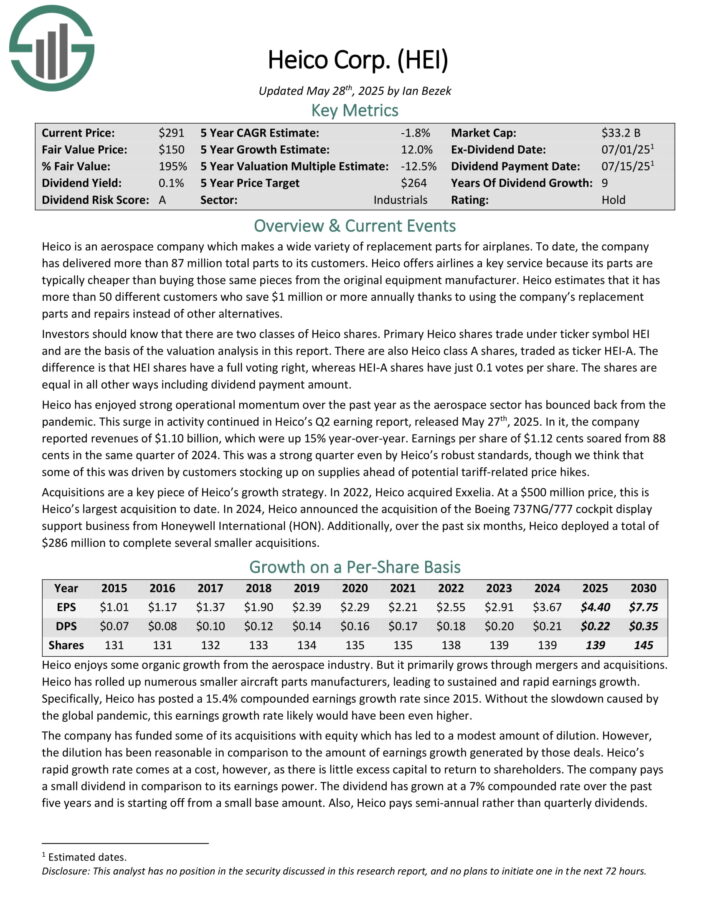

Excessive P/E Inventory #2: Heico Corp. (HEI)

Heico is an aerospace firm which makes all kinds of substitute components for airplanes. So far, the corporate has delivered greater than 87 million whole components to its clients.

Heico affords airways a key service as a result of its components are sometimes cheaper than shopping for those self same items from the unique gear producer.

Heico estimates that it has greater than 50 completely different clients who save $1 million or extra yearly because of utilizing the corporate’s substitute components and repairs as an alternative of different options.

Heico’s Q2 incomes report was launched on Might twenty seventh, 2025. The corporate reported revenues of $1.10 billion, which had been up 15% year-over-year.

Earnings per share of $1.12 cents soared from 88 cents in the identical quarter of 2024. This was a powerful quarter even by Heico’s sturdy requirements, although we expect that a few of this was pushed by clients stocking up on provides forward of potential tariff-related worth hikes.

Click on right here to obtain our most up-to-date Positive Evaluation report on HEI (preview of web page 1 of three proven under):

Overvalued Dividend Inventory #1: Wingstop Inc. (WING)

Wingstop is headquartered in Addison, Texas and franchises and operates eating places underneath the Wingstop model.

On April 30, 2025, Wingstop Inc. reported its monetary outcomes for the fiscal first quarter ended March 29, 2025. Thecompany achieved whole income of $171.1 million, marking a 17.4% enhance in comparison with the identical interval in 2024.

System-wide gross sales grew by 15.7% to $1.3 billion, pushed by a document 126 web new restaurant openings, representing an 18% web new unit progress. Home same-store gross sales skilled a modest enhance of 0.5%, whereas company-owned home same-store gross sales grew by 1.4%.

Internet earnings surged by 221% to $92.3 million, or $3.24 per diluted share, primarily on account of a $97.2 million achieve from the sale of Wingstop’s non-controlling curiosity in its United Kingdom grasp franchisee, Lemon Pepper Holdings, Ltd.

Adjusted web earnings stood at $28.3 million, or $0.99 per diluted share, surpassing analyst expectations of $0.87 per share. Adjusted EBITDA elevated by 18.4% year-over-year to $59.5 million.

Click on right here to obtain our most up-to-date Positive Evaluation report on WING (preview of web page 1 of three proven under):

Closing Ideas

The inventory market, as measured by the S&P 500 Index, is considerably overvalued proper now utilizing the Shiller P/E ratio.

Because of this, buyers could also be thinking about realizing which shares are overvalued on this market, and might be candidates to promote.

If you’re thinking about discovering high-quality dividend progress shares and/or different high-yield securities and earnings securities, the next Positive Dividend assets shall be helpful:

Excessive-Yield Particular person Safety Analysis

Different Positive Dividend Sources

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to help@suredividend.com.